Fiat vs. stablecoin cards: what the difference means for your business

Key takeaways

- Stablecoin card programs can go live in 2-3 months vs. 6-18 months for fiat programs

- Rain’s daily onchain settlement with card networks cuts partners’ collateral requirements significantly compared to the multi-day float required for fiat programs

- Rain-issued programs scale across geographies through a single integration, so partners are not required to rebuild in each market

- The benefits apply to any business looking to launch card programs, not just crypto-native companies

The default for businesses looking to launch a card program has long been the fiat-backed model, but that’s starting to change.

Stablecoin card programs are gaining traction, and not just from crypto-native companies. Fintechs, payroll providers, and global apps that once opted for traditional fiat setups are starting to consider an alternative model, and for good reason.

For cardholders and merchants, stablecoin-backed cards and fiat-backed cards are nearly identical. Transactions are seamless, acceptance is unchanged, and nothing about the payment flow feels new or unfamiliar.

The differences are structural, and they show up in the places that matter most to a business, like how much capital a program ties up, how long it takes to launch, and what it takes to expand internationally. The decision to go with a stablecoin or fiat model shapes the entire economics and footprint of a program from day one. Here’s how:

The stack: who's behind a card program

While fiat and stablecoin programs differ at the ledger and settlement layers, both are built on top of the same card network infrastructure. Let’s get to know these key components before explaining the differences:

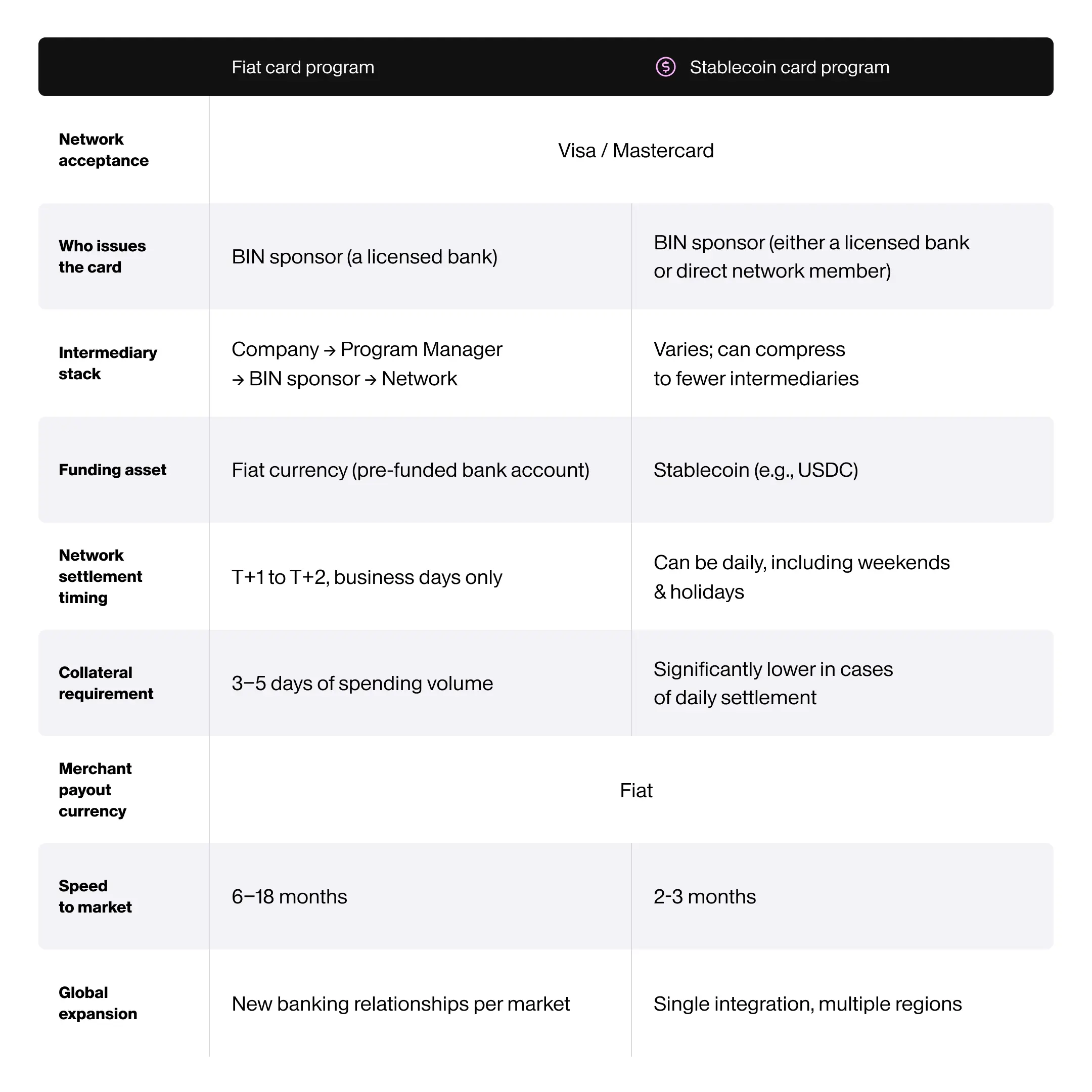

- The card network: Payment networks, like Visa and Mastercard, set the rules. They maintain the acceptance infrastructure, facilitate settlement between card issuers and merchants, and authorize transactions. To issue cards that work on the network, companies need to be a licensed network member, which comes with capital requirements, compliance standards, and other ongoing obligations.

- The BIN sponsor/issuing bank: Every card has a Bank Identification Number (BIN), which is the first six to eight digits on the card. BINs are assigned to licensed entities that are network members.

- The program manager: Between your company and the BIN sponsor, there is often a program manager. This is a third-party team that handles technical integration, card management, branding, and day-to-day operations.

Key differences between stablecoin & fiat programs

Difference #1: settlement and reserve requirements

It makes sense to start with the settlement layer, because this is the biggest economic burden on a business.

In a traditional fiat card program, a company must maintain a pre-funded balance, known as an FBO (“for benefit of”) account, with their issuing bank. Settlement with the card network typically takes two business days. Because of that lag, the company has to keep three to five days of projected spending volume in reserve at all times.

Rain’s card programs operate on a different timeline, from both the fiat model and other stablecoin-powered models. Rain settles with the network in stablecoins every day, including weekends and holidays. Since funds move daily, partners don’t need to pre-fund several days of spending, and capital reserve requirements drop significantly.

Rain's integrated virtual accounts and onramps allow partners to fund programs in stablecoins or fiat currency, so businesses that want to benefit from the efficiencies that stablecoins provide without holding stablecoins themselves have the option. This setup is particularly helpful for companies that want to modernize their card infrastructure without changing how they manage their existing finances.

This is one of the most significant benefits of a stablecoin-backed model. If two card programs can produce a similar end-user experience, but one requires materially less idle capital to support settlement, the difference goes beyond a technical distinction and becomes an economic advantage.

Difference #2: program expansion and USD access

Issuing cards globally is one of the most strategic ways a business can expand its financial offerings, particularly when it comes to high-demand US dollar-denominated cards. But just as settlement infrastructure can be a barrier to entry, the expensive and complicated process of expanding internationally can be prohibitive for businesses.

In markets around the world, businesses and consumers actively seek access to dollar-denominated spending, but because most fiat programs are effectively limited to a US market, there are few options.

The reason is structural. Fiat programs are often built on local banking infrastructure, and many banks in international markets cannot support USD-denominated card programs. Foreign currency exchange regulations and limited access to the US dollar clearing system make running these programs expensive and challenging.

Even when international banks can offer a USD-denominated card program, there are unique underwriting timelines, capital requirements, and approval processes in different regions. Companies with international programs also need to maintain pre-funded FBO accounts in each country.

Stablecoin infrastructure can offer a different path. Because reserves can be held in dollar-backed stablecoins rather than relying entirely on local fiat banking infrastructure, a stablecoin-backed card program can be designed to scale across markets more efficiently. That does not remove compliance obligations or local considerations, and it should not be framed as though it does. What it can do is reduce some of the fragmentation that makes conventional fiat expansion so operationally heavy.

Rain holds network membership and operates across multiple regions through a single integration, so a program that launches in one market can extend to others without rebuilding from scratch.

For companies thinking about the addressable market, global demand for dollar cards isn’t a future opportunity. It exists today, and it’s largely underserved because the fiat infrastructure required to reach it is too fragmented and slow to build. Stablecoin card programs can streamline the process, giving businesses a faster path to expansion.

Difference #3: speed to market

Speed to market is another area where the difference between fiat and stablecoin programs becomes tangible.

With a fiat model, businesses are constrained by the fragmented timelines of their various partners. Even before implementation begins, businesses can spend two to three months on finding and contracting a program manager. Bank underwriting adds more time, and the issuing bank won’t advance the program until compliance infrastructure is in place and reviewed. When programs need to raise venture debt or enlist a credit facility to fund FBO accounts, the process is extended even further.

Stablecoin card programs compress this timeline because the infrastructure provider can absorb much of the stack. When the provider holds direct card network membership, like Rain, a separate BIN sponsor and program manager aren’t necessary.

Stablecoin programs have the same compliance requirements, but fewer interdependent partners means those processes can run in parallel rather than sequence. Instead of coordinating multiple institutions with separate timelines, companies can move forward through a single integration.

In card issuing, speed is leverage. The faster a program goes live, the faster it starts generating revenue, learning from users, and compounding growth.

What stays the same

For all of these differences, a lot of the core card experience stays the same, and that is an important part of the appeal. A stablecoin card is not a different category of financial product, it’s just built on different infrastructure.

Similarity #1: compliance requirements and risk mitigation

A stablecoin-backed card program is not a shortcut around the obligations that come with issuing financial products. Businesses are required to collect customer identification through Know Your Customer (KYC) and Know Your Business (KYB) procedures when onboarding new cardholders. Anti-Money Laundering (AML) monitoring and Suspicious Activity Report (SAR) filing requirements under the Bank Secrecy Act apply equally.

Stablecoin card programs carry the same fraud and financial crime risks as traditional fiat programs; card sharing, credential theft, and unauthorized use aren’t unique to either model. What’s required to manage those risks is also the same. Programs must screen customers at onboarding through a Customer Identification Program (CIP), verify beneficial ownership for business accounts, and apply sanctions screening against authoritative sources like OFAC and card network requirements. Ongoing transaction monitoring and fraud prevention efforts are essential elements of both programs.

Similarity #2: the card experience

One of the biggest strengths of stablecoin card programs is that they do not change the cardholder or merchant experience.

When someone uses a stablecoin card to buy groceries, pay for ads, or book a flight, the merchant is not being asked to accept stablecoins or adopt new payment infrastructure. At settlement, the merchant receives fiat through the normal network flow, with no changes to their existing process required. Likewise, the cardholder does not need to understand anything about the settlement mechanics in order to use the card; they just tap or swipe as normal.

Stablecoin card programs carry the same consumer protection obligations as fiat programs.

Picking the best program for your business

For a long time, fiat card programs have been the default choice, and in many cases that was simply because they were the established path. But established does not always mean optimal.

The stablecoin model not only gives businesses a new option for funding a card program, but also offers a totally different economic structure for launching and scaling the offering.

For companies thinking beyond a single market or expecting meaningful transaction volume, differences in reserve funding, timeline to launch, and expansion requirements add up. A reserve gap that looks manageable at low volume becomes a significant capital commitment as the program grows. A per-market launch process that seems acceptable for one geography becomes a serious constraint when the goal is five.

Finally, stablecoin card programs are not solely designed for crypto-native companies. The benefits of lower collateral requirements, faster launch times, and easier scaling are universal. With the right infrastructure provider, digital asset literacy is not a prerequisite for businesses or cardholders. If you’re ready to learn what a stablecoin-backed card program can unlock for your business, let’s talk.