Why would I use Rain over other corporate cards?

Why would I use Rain over other corporate cards?

If you find outdated infrastructure is holding back traditional fintech products that make it difficult to access funds, you need a credit card designed specifically for crypto native teams. Here, we explain why Rain’s cutting-edge technology and on-chain infrastructure help resolve common issues, allowing you to spend faster than you receive a 2FA text message from a centralized exchange.

What is Rain?

Rain is a corporate card built for crypto-native teams redefining modern finance. It offers the fastest, most direct payment method connecting Web3 companies with vendors. This card also eliminates fees, offering instant spending so vendors receive fiat, avoiding the regulatory risks of accepting crypto. It is the best solution for companies looking for a corporate spend management platform as it is customized for DAOs, protocols, networks, and projects in the Web3 space.

As a result, it seamlessly accommodates the unique governance and operation models of Web3 teams yet never compromises fiat interoperability at the merchant level. Rain is helping to empower the expansion of the digital money ecosystem worldwide and is available on Ethereum and Polygon mainnet with plans to expand.

Who should use Rain?

Because of Rain’s revolutionary design, it is the ideal spend management platform for Web3 teams. If you rely on fiat ecosystems to operate, it is available for teams using self-custody, institutional custody, and everything in between, with seamless access to essential business tools. It can also support international organizations.

Why is Rain better than other corporate cards?

Rain accesses real-world spending with your on-chain assets and is the only solution that does not require a centralized exchange, OTC Desk, or a bank account for use. All existing providers either convert assets into fiat for you to spend or need a bank account with a cash balance to access a credit line. Rain, on the other hand, is the only corporate card allowing you to cover your business expenses using your on-chain assets.

You can also easily streamline your finances with accounting software integrations for Quickbooks™ and Entendre™ leveraging over $750,000 in discounts from the top companies across Web3 and Web2, including:

- Quickbooks

- Zoom

- Alchemy

- Slack

- Airtable

- Notion

Is Rain a credit or debit card?

Rain provides native credit and repayment support for stablecoins like USDC and is on Ethereum and Polygon mainnet. Because it operates on the credit rails, it acts as a credit card, allowing you to use it for business expenses like reserving rental cars, booking flights and accommodations, and purchasing from other vendors, something you can’t do with many competing debit cards.

You have a credit limit set against the value of your on-chain assets, such as USDC, allowing you to plan your monthly spending. A significant difference is that your funds aren't debited from your account after each transaction like a debit card and instead are payable at the end of each month.

Why is Rain the better corporate card for teams?

Simply put, you set the limits for your team and their cards to help control spending. You also have an automated account and reconciliation option providing granular memos and receipt capture so you can consolidate your on-chain spending effortlessly. Rain can also manage individual team budgets, allowing you to set up sub-accounts for each team.

If your Web3 company needs an easy way to monetize and spend crypto, Rain is the best corporate card solution.

What are the benefits of using Rain crypto corporate cards for expenses like corporate travel?

What are the benefits of using Rain crypto corporate cards for expenses like corporate travel?

If your crypto company or foundation wants to leverage crypto currency to help manage expenses, it can come with a hefty fee, not to mention delays. In fact, when relying on exchanges and OTC partners to manage your fiat spending, fees can range from 1-10% for each transfer. Here, we share the benefits of using the Rain credit card to cover expenses without worrying about delays and costly fees.

What is a Rain credit card?

Rain credit cards come with a state-of-the-art corporate spend management platform designed to accommodate the unique governance and operation models of Web3 teams. Although traditional fintech products are held back by outdated infrastructure, Rain leverages on-chain infrastructure to drive efficiency for digitally native teams. Rain members can cover expenses in real life quicker than alternatives in the market.

Why is Rain best for your expenses?

Rain provides instant and seamless access to spending without any OTC margin or spread, saving your team an average of 3% to 4%. You can use your Rain card anywhere VISA is accepted, allowing you to spend your digital assets at merchants around the world. Although OTC trading is convenient when swapping larger sums fast and confidentially, it makes no sense for crypto companies to depend on an OTC desk to access funds to cover basic expenses like corporate travel.

Also, the Rain credit card acts like a traditional credit card, making it better for booking flights, securing accommodations, or reserving a rental vehicle for corporate travel. Perhaps best of all, Rain members have until the end of the month to pay their bill, meaning funds, tokens, and assets aren't debited from your account after each transaction like a debit card. As a result, crypto companies often find they maintain better control over their digital asset spending while managing cash flow deficits more effectively.

How does the Rain credit card help you save money?

In hand with an average savings of 3% to 4%, Rain also helps you save in several other ways, including:

- Users have access to opportunities for over $750,000 in savings through Rain partnerships

- You can simplify your accounts payable without the need for data entry, reducing errors and repetition that cost money to manually enter, track, and correct

- Effortless invoice payments allow you to pay at the end of each month instead of debiting crypto for each transaction to help provide a break when you experience cash flow challenges

- You also streamline accounting functions with seamless integration with Quickbooks™ and Entendre™

- With easy management of sub-accounts for individual team budgets, you become more aware of spending across your organization to make informed financial business decisions

- You can consolidate your on-chain spending using automated accounting, including quick reconciliation and receipt capture

- Your accounting team can onboard bookkeepers and accountants to accurately document and tag transactions to simplify corporate accounting and reporting

Rain credit cards eliminate unnecessary fees, offer instant spending opportunities using your crypto assets, and ensure vendors receive fiat without the regulatory risks of accepting crypto.

What happens if I lose my card and need another one?

What happens if I lose my card and need another one?

When you need a global credit card solution that merges your digital assets with fiat ecosystems, Rain’s state-of-the-art platform makes crypto transactions easy. However, if team members misplace their physical cards, it’s essential to understand what steps you should take to ensure your account remains secure and accessible. Here, we explain what happens when you or a team member loses their card and needs another one.

How do cardholders request a new card and inform Rain of potential issues on the account?

Rain enables fast replacement of lost physical cards with delivery available worldwide. Your Company Administrators can request replacements through your Rain Account using the Company User’s full legal name and identifying and contact information such as date of birth.

It is vital to inform Rain of lost or stolen cards immediately so they can take appropriate measures to prevent unauthorized transactions. Because replacement cards usually have new account numbers, be sure to update the Rain Card on file for any scheduled or recurring payments. If you are worried about fraudulent activity, contact support@raincards.xyz or call the phone number on the back of your Rain card.

How does the granular spending control process work?

When your Company Administrators request cards for new users, they can assign specific restrictions for each user. For example, some users might only need a card to use for vendor transactions with specific merchants, while other users might require a particular expiration date because they are contract employees. These special restrictions can be assigned to yourself or a teammate, including setting spending limits. These limits can be based on daily, weekly, monthly, yearly, or all-time limits to suit your expense budget or card user functions.

What is Rain’s dispute process for addressing unauthorized charges?

If you did not authorize a charge that you see on your card, you should promptly reach out to support@raincards.xyz or call the phone number on the back of your Rain card. As with any card, the holder is responsible for reviewing Periodic Statements to identify any Charges you believe are unauthorized. If the dispute is based on your belief a Charge was unauthorized, you can initiate a Chargeback through your Rain Account. It is critical to review your statements promptly, as you have 60 days after the disputed Charge is posted on your Periodic Statement to voice your concerns.

Rain might request additional details on the transaction and review the disputed Charge once they have collected the necessary information. If a charge dispute is pending, it is still considered outstanding and due on the date indicated on your Periodic Statement. Once the dispute is resolved in your favor, the amount will be credited to your Rain Account on either the current or a future Statement. You must make your full payment to avoid fees, a reduction in spending limits, or suspension of your Rain account.

Rain makes it easy to request a replacement for a lost card, set granular spending controls to reduce fraudulent activity, and dispute any unauthorized charges you see on your Periodic Statements.

Can my Rain credit card be added to my smartphone wallet?

Can my Rain credit card be added to my smartphone wallet?

'Rain' credit cards acts as a safe bridge between your cryptocurrency holdings and everyday transactions providing secure spend management from your crypto wallet with no exchange or bank account required.

But to make how you spend your funds even more seamless, you may be wondering ‘Can my Rain Credit Card be added into my smartphone's digital wallet?’

The short answer is, *yes*, your Rain card can be added to many mobile wallets.

This ensures you can enjoy the convenience and security of mobile payments with the cutting-edge features of the Rain Credit Card.

However, let's delve deeper to provide a clearer picture of compatibility across Apple and Android:

For Apple users, there is a minor hiccup.

If your company is incorporated in the U.S chances are you can add your Rain credit card to your apple wallet. However, due to some constraints imposed by certain wallet partners, not all Rain cards can be synced with Apple Pay. Apple, as a platform, has its specific set of requirements, and sometimes this may lead to limited compatibility with certain third-party services.

However, for Android users, there's good news.

Rain credit cards can be utilized in conjunction with mobile wallets on the Android stack, including Google Pay. This implies that irrespective of the Rain card you possess, if you're on the Android platform, you can effortlessly integrate it with your digital wallet. Such broad compatibility is a testament to Rain's commitment to making crypto transactions as effortless as possible.

The integration of Rain with mobile wallets, especially on the Android platform, offers myriad benefits. First, it bolsters security. Mobile wallets, like Google Pay, employ a host of security measures, such as tokenization, which replaces your card's actual number with a unique code for each transaction. This ensures your real card details are never exposed, providing an added layer of protection against potential credit card fraud.

By linking your Rain credit card with your mobile wallet, you enjoy the ease of tapping your phone to pay instead of fishing out your physical card. This not only accelerates the payment process but also means one less item to carry when you're on the move.

In conclusion, while there are certain limitations with its integration into Apple Pay which should not affect most users in the USA, Android users have the green light across the board.

If you haven't already, consider adding your Rain card to your smartphone wallet and experience a seamless, secure, and swift transaction journey.

Can Rain and credit card offramps be used safely by crypto foundations?

Can Rain and credit card offramps be used safely by crypto foundations?

Many crypto foundations struggle with the risks of using a centralized exchange to convert crypto into fiat. Rain and credit card off-ramps could be the answer to avoid a complicated process that stems from the flow of economic value between crypto and cash funds, not to mention risks associated with the U.S. Securities and Exchange Commission (SEC). Here, we explain how your crypto foundation can safely use Rain and credit card off-ramps without the need for a centralized exchange.

What are offramps?

Crypto off-ramps simplify the flow from crypto to fiat money so you can cash out of crypto and have money in the bank, so to speak. You can exchange your crypto quickly and safely, so you can bridge the gap between cash and modern forms of currency, allowing your company or foundation to reduce friction, time, and money associated with legacy fiat rails.

What is Rain?

Rain is a spend management platform revolutionizing interoperability for digital assets with the fiat ecosystem. As a result, crypto foundations have seamless access to fiat, making funding available for your projects using on-chain assets via virtual cards without the need for a centralized exchange.

What does Rain support?

Rain supports a variety of corporate structures including, foundations, DAOs, holding companies, etc.

How are Rain and credit card offramps used?

Rain can on-board your foundation and its employees, contractors, and contributors directly and safely. Because crypto was designed to remove the barriers and make it easier to move value to access funds between economic models, using Rain or credit card off-ramps brings traditional money and the decentralized web together.

With Rain, you get access to a credit card platform that can be used at merchants worldwide. You get instant access to spending in real life without having to off-ramp funds into fiat first. As a result, your project has a seamless way to continue to utilize your self-custody assets without having to rely on off-ramping or storing funds with a bank partner.

What makes Rain better for foundations?

Foundations are a relatively new corporate structure which has gained popularity with crypto native projects and protocols. Since the corporate structure is fairly new and requires a set up in jurisdictions which support this type of structure, a lot of foundations tend to have a difficult time getting access to bank accounts and bank partners. Similarly, foundations have challenges getting reliable access to exchanges to help off-ramp crypto tokens as exchanges usually require a bank account to liquidate money into. With Rain, you are able to access corporate spend management tools without needing a bank account or an account with a centralized exchange to interface with the platform.

Rain is the most direct way to access on-chain assets without converting them into fiat for spending or needing a cash bank balance to access a credit line. It is the only solution that doesn't require a centralized exchange, OTC Desk, or a bank account, so foundations can use Rain to pay for expenses using their on-chain assets. Because it operates on the credit rails, it can be used more like a credit card, with a credit limit set against the value of on-chain assets.

USDwtf? Why interoperability matters more than the letter

Everyone’s minting branded dollars.

From PayPal and Fidelity to Walmart and Amazon, some of the biggest names in finance and consumer commerce are developing and announcing their own versions of tokenized money. The landscape is quickly maturing, and it can be disorienting.

For enterprises starting to think seriously about stablecoins, today’s environment raises questions. Are branded stablecoins actually the future of money, or are we just reinventing gift cards on a blockchain?

The honest answer is that it depends, and not on the branding or the institution issuing the token. The success of any given stablecoin usually comes down to one factor: whether or not it can actually move. Interoperability is the difference between a real currency and a closed-loop instrument that only works where it was issued.

Before I get into the details of interoperability, let me first address why so many dollar-backed tokens are coming on the scene in the first place. It’s mostly because stablecoins are a compelling business.

They move at high velocity onchain while the underlying reserves remain largely static, allowing issuers to earn yield on collateral even as value circulates rapidly through the economy. Why wouldn’t banks and large brands be drawn to a new, low-risk revenue stream?

Over the past year, this has resulted in some of the largest enterprises rushing to issue a press release about their branded stablecoin. But the days of PR coming first and utility being an afterthought are fading.

Why? For starters, history shows that technology doesn’t scale just because it exists, or even because it offers a superior way to do something. Mainstream adoption of stablecoins will depend on people being able to use the new technology conveniently.

As stablecoins mature, users will care less about whose stablecoin they are holding and more about whether it works everywhere they need it to. The future is not a world where consumers consciously juggle half a dozen branded dollars. It’s a world where value moves seamlessly, often without the user ever knowing what letters were appended to their token behind the scenes.

Realistically, there will be some branded stablecoins that reach mainstream recognition. In some cases, adoption and scale can be forced. If a major retailer, like Amazon or Walmart, makes its own stablecoin the only accepted form of payment, people will use it.

But there are very few players dominant enough to demand adoption in this way, and, at the end of the day, a stablecoin that’s only usable for certain transactions isn’t real money. At best, it’s a yield mechanism for the brand and a poor UX for the consumer.

The future can, and will, support dozens of branded stablecoins unknown to consumers and a few branded stables that have widespread awareness, but only if interoperability is prioritized. Just look at web adoption.

The internet didn’t succeed because everyone used the same server. It scaled because protocols made everything interoperable. Money must follow the same path. The goal isn’t to eliminate choice, it’s to make choice invisible.

So, how do we unlock this future? At the end of the day, interoperability comes down to infrastructure.

In practice, it requires native integrations with issuers, clean mint and redeem paths, reliable onramps and offramps, and payment rails that work across onchain and offchain environments.

That’s where Rain comes in. Our focus is payment utility. Our goal is to turn any stablecoin into real-world spendable value, through cards, payouts, and direct movement between onchain and offchain economies.

In a multi-stablecoin world, that layer matters more than the brand behind the stablecoin. The less users have to think about what kind of dollar they are holding, the more stablecoins can behave like real money.

Stablecoins are becoming foundational financial infrastructure.

As that happens, the winners will not be the loudest brands or the most clever tickers. They will be the systems that make money interoperable, spendable, and forgettable.

In the long run, the letter matters less than whether the dollar works everywhere.

The future of agentic commerce is built on stablecoins

The next phase of AI is agentic commerce. Autonomous actors aren’t just going to be doing research, they are going to be taking action, and that means moving money.

AI agents are already searching, initiating, and independently completing financial transactions, sometimes continuously. As the software improves and models become more reliable, agentic commerce will only become more common. Businesses are going to increasingly rely on these tools to simplify operations. The problem is today’s payment infrastructure was never designed for agentic actors.

Traditional systems come with human-centric authorization processes, like logins and multi-factor authentication. Fee structures are designed for large, infrequent payments, not the constant programmatic transactions AI agents need to execute. Delayed settlement undermines autonomous decision making, slowing the entire process.

Stablecoins resolve many of these friction points by design. By cutting out intermediaries, they settle faster and come with fewer fees than traditional rails. Stablecoins are programmable, so users and businesses can customize spending conditions, timing, and limits before transactions take place.

This matters most when agents make frequent, granular decisions and purchases. Micropayments are a clear example. An AI research agent may be providing answers in real-time, which requires queries across several data sources, queries that could cost mere cents. Via traditional credit card networks or ACH, sending such small payments is effectively impossible, and the fees alone are higher than the transfer value.

Stablecoins provide a solution. By removing fixed, per-transaction fees, value can move quickly and efficiently. Value moves directly between wallets on global, always-on infrastructure, removing intermediaries and per-hop fees. With stablecoins, it doesn’t matter if an agent sends $100 or $0.001, the incremental cost doesn’t scale the same way it does on traditional rails, making the continuous microtransactions that power AI tools possible.

On fiat rails, rules live outside the money: spending limits, compliance checks, and approvals are layered on top, and enforced by intermediaries after transactions are attempted. Stablecoins flip the model, allowing the rules to be embedded directly into how money is used, not just how it’s monitored. AI agents don’t need to ask for approval or wait for reconciliation, it happens automatically because the controls are built into the flow of payment.

AI companies building agentic commerce tools need an infrastructure provider that can implement stablecoin rails. And companies looking to improve efficiencies with agentic payment tools need a partner that can support this model without forcing them to rebuild their entire payments stack from scratch.

At Rain, we partner with teams to connect stablecoin rails to real-world commerce with compliant, stablecoin-backed cards, so agents can execute transactions and businesses can retain the control and visibility they need.

We see where payments and AI are headed, and we’re building the infrastructure to support the change. If you’re ready to explore new solutions, get in touch.

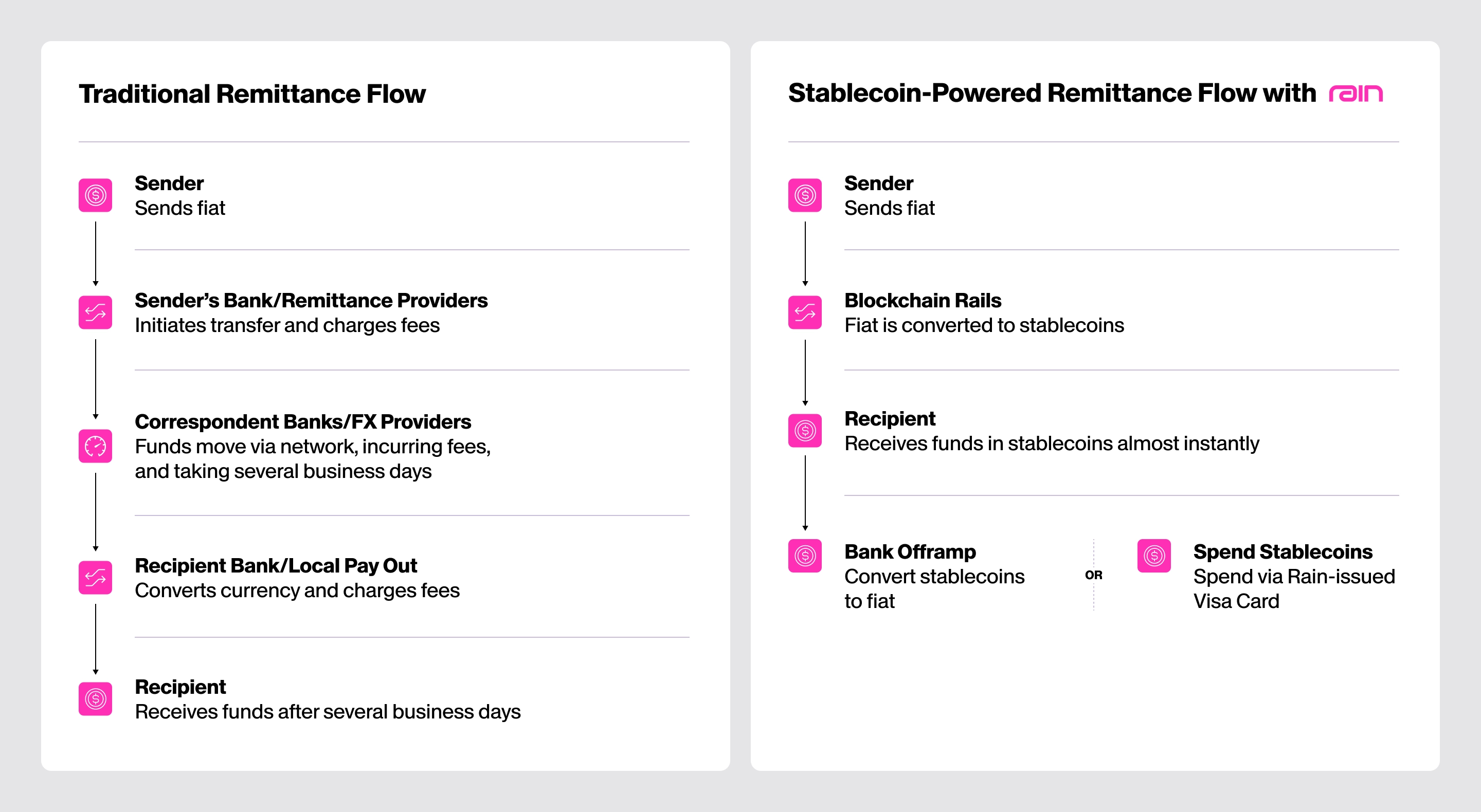

Spendable remittances that move in seconds and work on arrival

Every year, hundreds of billions of dollars are sent across borders. These payments are lifelines for families, support systems for communities, and essential income for workers across the world. In 2024, global remittance flows hit a record $905 billion.

These payments are critical, yet the system that supports them still runs on outdated rails, riddled with delays, fees, and friction points.

Stablecoins offer a clear solution. They reduce costs, settle instantly, and allow money to move over programmable, borderless infrastructure. They’re not limited to banking hours, and unlike traditional rails, don’t rely on a patchwork of third-party intermediaries.

Stablecoins upgrade the infrastructure, but the assets have to be spendable to provide real utility for users. That’s where Rain comes in.

Why stablecoins are changing the game

For remittance providers, stablecoin rails offer a meaningful upgrade to the economics, operations, and reach of the business.

Traditional remittance models require managing float across multiple banking partners, currency corridors, and regulatory zones. That means maintaining costly pre-funded accounts, coordinating with correspondent banks, and building out complex treasury infrastructure, all while navigating volatile FX markets.

Rain offers remittance platforms a simpler path forward:

- Lower treasury and liquidity costs

Stablecoins reduce the need for capital to sit idle across dozens of local accounts. On-demand funding and real-time settlement optimize float and unlock working capital. - Reduce cross-border settlement costs

Stablecoin rails eliminate intermediaries and costly banking hops. That means fewer layers of fees, faster reconciliation, and less friction with local payout partners. - Capture more of the FX spread

Instead of absorbing unfavorable exchange rates or relying on third parties for conversion, remittance platforms can execute FX when and where it makes the most sense. That leads to better margins and more control. - Reach new markets without legacy infrastructure

Stablecoins open up corridors that are underserved by traditional banks. With Rain, remittance providers can launch in more regions without building new local bank relationships or opening physical branches.

Rain helps platforms integrate this shift without the lift. With one stack, you get programmable stablecoin flows, integrated compliance, Visa card issuance, and on and offramps that work across cash, bank, or wallet endpoints.

A better model: spendable remittances

Even when money moves fast, the last mile still slows people down. Recipients often wait on conversions, navigate across payout apps, or visit physical agents to access their funds.

That’s a real problem, especially when people need to cover urgent expenses like rent, groceries, or transportation.

Rain fixes the last mile. Our infrastructure turns remittances into ready-to-spend value. By moving funds onchain, senders avoid the high fees and unfavorable exchange rates that come with most traditional remittance systems. That means no hidden FX mark‑ups, lower transfer costs, and substantially more value reaching the recipient.

The process with Rain is simple: funds are onramped into stablecoins, stored securely in a wallet, and made instantly usable via a Rain-issued Visa card accepted by more than 175 million merchant locations worldwide.

Because the card is integrated directly into the remittance flow, value stays on the provider's platform instead of leaking out through offramps. Providers can earn yield on the stablecoin balances held and interchange on every card swipe, so the last mile becomes a source of revenue rather than a cost. Recipients gain too, since spending no longer depends on offramping into local currency first. They use their funds the moment they land.

No extra steps. No waiting. Just real-world utility, available instantly.

Here’s how Rain’s stablecoin-powered alternative compares to legacy rails:

From remittance to real spend: Rain x Zar

Across Asia, Africa, and Latin America, cash still drives the economy. People rely on networks of corner shops, airtime vendors, and mobile money agents to move everyday value. In 2024, over $1.6 trillion flowed through mobile money accounts via 28 million registered agents.

Zar is helping modernize the system. Through their platform, users in Pakistan can receive remittances from abroad directly in stablecoins, providing consumers with faster settlement, dollar stability, and lower fees compared to legacy remittance methods.

But access to digital dollars is only part of the solution.

With Rain, those stablecoins become immediately usable. Zar users can link their wallet to a Rain-issued Visa card and spend their funds right away. No offramps. No waiting.

Zar is expanding access for the unbanked. Users can visit a participating corner shop, hand over physical cash, and have it converted into stablecoins, deposited directly into the same wallet they use to receive remittances. This gives people a way to store value in dollars, even without a bank account.

Together, Rain and Zar deliver something the industry has long struggled to achieve: a remittance experience that actually works on arrival.

The full circle: onramps, spendability, and offramps

Rain has always supported the full value loop, from fiat onramps and onchain transfers to instant card-based spend. Now, we’re unlocking a new layer of global access: cash pickup through Western Union.

With our new integration into the Western Union Digital Asset Network, users can now convert stablecoin balances into local currency and pick up physical cash at thousands of Western Union locations worldwide, making remittance payments more flexible and accessible.

Whether someone prefers to tap a Rain-issued card or walk away with cash, it all happens from a single wallet.

With Rain, you get:

- Fiat onramps via ACH or wire with conversion to stablecoins and funding to a wallet.

- Wallet infrastructure for users to store, manage, and access stablecoins.

- Programmable cross‑border transfers via API, with real‑time status and rich metadata for audit and reconciliation.

- Immediate spendability through Rain‑issued physical and virtual cards that your recipients can use anywhere Visa is accepted, reaching 175M+ merchant locations globally.

- Local‑currency offramps to bank accounts when cash settlement is required.

- Integrated compliance (KYC/AML) embedded in the end-to-end flow.

- Value stays on-platform when recipients spend from an integrated card, letting providers earn yield on balances and interchange on swipes while sparing recipients the offramp step.

The bottom line

Remittances should be fast, cost-effective, and ready to use the moment they land. Rain makes that possible.

By removing friction at the point of use, Rain gives recipients instant access to funds and enables remittance providers and payout platforms to move money more efficiently from send to spend.

Ready to modernize your cross-border infrastructure and unlock new value for your users and your business? Let's talk.

Rain raises $250M Series C to scale stablecoin-powered payments infrastructure for global enterprises

Led by ICONIQ, the round brings Rain’s total funding to over $338M and values the company at $1.95B — up more than 17x in just 10 months

The new funding enables Rain to scale its global, compliant footprint, deepen platform capabilities, and invest in new products that redefine how payments work worldwide

NEW YORK — January 9, 2026 — Rain, the enterprise-grade infrastructure for stablecoin-powered payments, today announced a $250 million Series C funding round led by ICONIQ, with participation from Sapphire Ventures, Dragonfly, Bessemer Venture Partners, Galaxy Ventures, FirstMark, Lightspeed, Norwest, and Endeavor Catalyst. The round values Rain at $1.95 billion, brings the company’s total funding to over $338 million, and comes just four months after its Series B and 10 months after its Series A.

Stablecoins have rapidly evolved from a speculative corner of crypto markets into one of the largest value-transfer rails in the world. The next phase of adoption is about making tokenized money the default way that businesses move funds and consumers get paid, save, and spend. Crossing that chasm requires infrastructure that lets enterprises shift to onchain payment rails while preserving the familiar experiences their users already trust. Rain’s technology is built to do exactly that.

“Stablecoins are quickly becoming the way money moves in the 21st century, but adoption by users worldwide requires cards and apps that just work,” said Farooq Malik, CEO & Co-founder of Rain. “In the last year, our active card base has increased 30x and our annualized payment volume has increased 38x, but we’re still in the early innings. This funding lets us bring that infrastructure to new markets and help additional enterprises go live and scale quickly everywhere.”

Rain’s end-to-end payments platform allows companies to work with a single partner to launch compliant stablecoin cards that work everywhere Visa is accepted, offer rewards, convert fiat into stablecoins, power secure wallets, and facilitate payouts. Today, Rain’s technology facilitates more than $3B in annualized transactions for over 200 partners, including Western Union, Nuvei, and KAST. Programs built on Rain can reach over 2.5 billion people and power everything from everyday consumer purchases like a morning coffee or airline tickets, to critical business expenses such as cloud services and digital advertising.

“We believe we’re witnessing a shift from legacy payment networks to programmable digital-asset infrastructure, and there is a brief window to help define the default platform enterprises will rely on,” said Kamran Zaki, Partner at ICONIQ. “In our view, Rain has a rare combination of full-stack technology, regulatory readiness, and real-world scale. Their focus on making tokenized money mainstream, rather than a niche financial experiment, may resonate and align with what large enterprises are looking for as they move from exploration to production.”

Rain will use the Series C capital to expand its presence in key licensed markets across North America, South America, Europe, Asia, and Africa, so partners can seamlessly launch compliant solutions around the world. The funding will also enable Rain to deepen its full-stack stablecoin payments platform, including through strategic acquisitions, and to invest ahead of the curve in new products that make stablecoin-powered payments feel invisible to businesses and consumers.

Wachtell, Lipton, Rosen & Katz served as legal advisor to Rain on its Series C financing.

About Rain: Rain is the global stablecoin payments platform for enterprises, neobanks, platforms, and developers. Its technology allows partners to move, store, and use stablecoins instantly and compliantly through global payment cards, rewards, on/offramps, wallets, and cross-border rails. As a Visa Principal Member, Rain issues cards that work anywhere Visa is accepted, powering millions of purchases in over 150 countries. Built natively for stablecoins and trusted by more than 200 organizations worldwide, Rain delivers secure, scalable infrastructure that makes money move freely and instantly around the world. Learn more at https://www.rain.xyz/.

About ICONIQ: ICONIQ is a global investment firm catalyzing opportunity through extraordinary community. Our venture and growth investment platform partners with visionaries defining the future of their industries to achieve uncommon outcomes. Drawing on the insights and connectivity of our extraordinary community, we support our portfolio companies’ success at every inflection point, from inception to IPO and beyond. Our robust portfolio includes Adyen, Airbnb, Alibaba, Alteryx, Airtable, Anthropic, Automattic, BambooHR, Braze, Canva, Chime, Coupa, Databricks, Datadog, DeepL, ElevenLabs, Figma, Gitlab, Glean, Groww, Netskope, Procore, ServiceTitan, Sierra, Snowflake, Writer, Zoom and 1Password, among others. For more information visit https://www.iconiqcapital.com/growth.

Read original press release here: https://www.prnewswire.com/news-releases/rain-raises-250m-series-c-to-scale-stablecoin-powered-payments-infrastructure-for-global-enterprises-302657084.html?tc=eml_cleartime

Media Contact:

Lucas Piazza

Marketing Lead, Rain

Rain expands Visa Membership into Asia-Pacific, advancing the reach of its global stablecoin payment infrastructure

Rain's expanded issuing footprint enables global consumer and corporate credit card programs across some of the world's most digitally active economies.

NEW YORK — March 24, 2026 — Rain, the enterprise-grade infrastructure for stablecoin-powered payments, today announced a major expansion of its Visa Membership into Asia-Pacific (APAC). Through Visa, a world leader in digital payments, Rain is expanding its card issuing footprint in the region, broadening its global infrastructure and allowing partners to launch and scale consumer and corporate credit card programs in some of the world's most digitally active economies, with initial launches expected in Q2 2026.

The expansion builds on Rain's existing issuing infrastructure and introduces a regulated presence in the region, strengthening the company's long-term issuing capabilities across APAC and enabling partners to launch and scale programs with greater regional stability. This milestone establishes Rain as one of the few stablecoin infrastructure platforms with direct Visa Membership supporting programs at this scale.

Asia-Pacific has emerged as one of the world's most active regions for digital asset adoption, consistently ranking among global leaders in stablecoin usage and home to some of the world's largest remittance corridors. According to the International Monetary Fund, the region accounted for more than $500 billion in stablecoin transactions in 2024, making it the second-largest region globally after North America.

"Businesses operating internationally should not have to stitch together multiple issuing partners and vendors just to launch a global card program," said Farooq Malik, CEO and Co-Founder of Rain. "Our expansion into Asia-Pacific allows partners to build and scale global programs through a single platform, while stablecoins improve how money moves behind the scenes."

The expansion unlocks a range of high-impact payment use cases across the region, including:

- Consumer and retail payments: Partners can launch Visa-branded card programs across APAC, with acceptance at over 150 million merchant locations worldwide. Stablecoins power settlement flows behind the scenes while preserving the familiar card experience for consumers.

- Instantly spendable remittances: APAC is home to some of the world's largest remittance corridors. Stablecoin-backed card infrastructure allows recipients to instantly spend remittance funds at Visa-accepted merchants worldwide, while keeping value within the provider's ecosystem and reducing reliance on costly cash-out and bank transfer flows.

- Corporate treasury and global payouts: Export-driven businesses across APAC can use stablecoin-backed card infrastructure to manage multi-currency treasury operations, fund corporate cards, and distribute payouts across global workforces and supply chains.

Rain's model keeps stablecoins simple for the end user. Cardholders transact as they normally would at millions of merchants worldwide, while stablecoins power efficient settlement flows behind the scenes. This architecture allows enterprises to modernize their financial infrastructure without requiring changes to consumer behavior or merchant acceptance.

"Visa is committed to enabling innovative partners and expanding global access to digital payments," said Nischint Sanghavi, Visa's Crypto Lead for the Asia-Pacific region. "Our collaboration with Rain reflects our focus on delivering secure, scalable payment experiences as digital assets continue to evolve."

This milestone marks the beginning of Rain's broader strategic buildout across APAC, with additional markets and program capabilities expected throughout 2026 and beyond. It builds on Rain's rapid growth and continued investment in borderless infrastructure, enterprise-grade compliance, and the systems that enable partners to launch and scale payment programs worldwide. As stablecoins become embedded within mainstream commerce, Rain remains focused on advancing the infrastructure that makes tokenized money spendable everywhere.

About Rain

Rain is the global stablecoin payments platform for enterprises, neobanks, platforms, and developers. Its technology allows partners to move, store, and use stablecoins instantly and compliantly through global payment cards, rewards, on/offramps, wallets, and cross-border rails. Rain issues cards that work at over 150 million merchants across 150 countries. Built natively for stablecoins and trusted by more than 200 organizations worldwide, Rain delivers secure, scalable infrastructure that makes money move freely and instantly around the world. Learn more at https://www.rain.xyz/.

Read original press release here: https://www.prnewswire.com/news-releases/rain-expands-visa-membership-into-asia-pacific-advancing-the-reach-of-its-global-stablecoin-payment-infrastructure-302722723.html?tc=eml_cleartime

Media Contact:

Lucas Piazza

Marketing Lead, Rain

lucas@rain.xyz

How to launch global card programs without starting over in every market

Scaling your product should get easier over time, not harder. But for most teams, expanding a card program internationally requires starting from square one in every new market.

Moving into a new country means finding a new issuer, adapting to new regulations, and dealing with one lengthy timeline after another. Progress slows just when momentum matters most.

Rain breaks that pattern. We’ve built the licensing, compliance, and stablecoin infrastructure so you don’t have to start from scratch in every new region. With a single integration, you can issue cards globally through a platform designed to work across borders and help your business scale.

The traditional model wasn’t made for global expansion

When it comes to issuing cards in a single market, the process is well understood, but far from easy. Teams still need to secure a BIN sponsor, integrate a processor, set up KYC and compliance workflows, and coordinate across multiple partners before going live.

After all that, when it’s time to expand, companies can’t just “copy and paste.” Teams that want to go global have to:

- Partner with a new issuer in every country or region

- Rebuild compliance flows

- Reintegrate wallets, KYC systems, and settlement rails

- Absorb longer timelines, higher costs, and greater regulatory risk

The result is a fragmented setup that’s expensive to maintain and difficult to replicate.

A platform that removes the roadblocks

Rain is designed to support expansion without fragmentation. With us, the process doesn’t have to restart with every new country.

For neobank KAST, partnering with Rain was about taking their existing card program global. The team wanted to expand into new countries, but redesigning their stack for each individual launch was impractical. With Rain, KAST was able to bring their program into new regions quickly, maintain consistency for users, and scout the operational overhead that typically slows international rollouts.

For companies launching a new program from the ground up, Rain’s approach is the same: deliver a full-stack that comes with one platform, one integration, and is designed to scale when you’re ready.

Stablecoins for settlement, fiat for users

Rain has secured the approvals needed to issue cards in dozens of countries. As a Visa Principal Member, we can issue directly and enable card programs that work at over 150 million merchant locations in more than 150 countries.

For users, that means a card that works exactly how they expect it would. Cardholders don’t need to hold crypto, and they won’t know stablecoins are powering everything on the back end.

Behind the scenes, Rain settles with Visa every single day – including weekends and holidays – using stablecoins. For Rain partners, that means reduced working capital and reserve requirements, while still allowing programs to be funded in fiat via wire, ACH, or SWIFT transfers.

Virtual and physical cards, out of the box

Rain supports both virtual and physical cards through the same API. Virtual cards can be added to Apple Pay and Google Wallet, making them ideal for immediate access or remote users. Physical cards are available in supported regions and fully customizable.

Whether you’re issuing spend cards for individual users or rolling out a corporate card program for a globally distributed workforce, Rain helps you deploy fast.

Built-in compliance and KYC

Every Rain-issued card program includes required KYC and AML workflows. We cover onboarding, identity verification, ongoing monitoring, and country-specific requirements, so you can stay compliant without having to build your own risk and ops stack.

Flexible by design

Rain is modular. You can use the full platform, including custody, wallets, compliance, and payments, or integrate only what you need alongside your existing systems. That makes it possible to:

- Add cards to existing user wallets

- Maintain control over branding, issuance logic, and customer service

- Expand into new markets without disrupting what’s already live

And as your needs evolve, you can introduce features like spend controls, rewards, or multi-currency support without reworking your core infrastructure.

Launch faster. Scale smarter.

We’ve seen teams spend years and significant capital building global card programs the hard way. Rain’s goal is to provide a better system.

With Rain, you can:

- Launch in new regions without sourcing a new issuer each time

- Simplify settlement and reduce capital overhead

- Issue cards immediately usable for real-world spending

- Customize and grow your program without losing visibility or control

Whether you’re a fintech expanding internationally or a Web3 platform making digital assets spendable, Rain provides the foundation to grow across markets.

The bottom line

Global expansion doesn’t have to mean starting over. With Rain, the infrastructure is already in place. The rails are ready. And your cards are good to go.

If you’re ready to scale without the slowdowns, let’s talk.

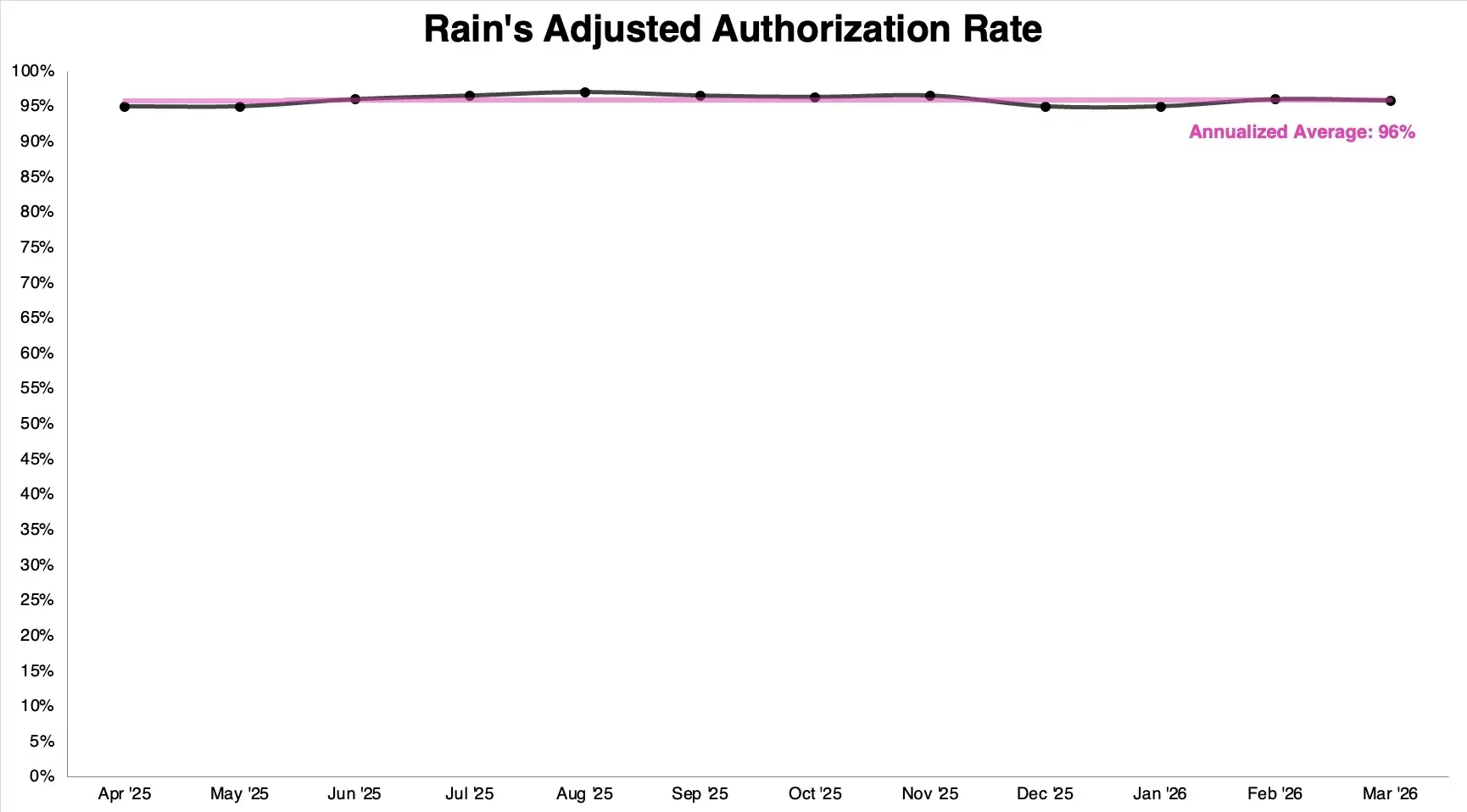

How Rain’s authorization rate is one of the highest across stablecoin cards

Authorization rate is a direct measure of how well a card program’s infrastructure performs in the real world.

A high authorization rate means things like fraud checks, balance logic, and merchant codes are working as intended. A low authorization rate signals issues, like misaligned risk models, poor network compliance, or technical malfunctions.

Multiple parties are involved in approving or declining a transaction, but for the card issuer in particular, maintaining a high authorization rate is a significant lift. Fraud detection and network compliance are two of the biggest drivers of authorization rate, and both are Rain’s responsibility.

Over the past twelve months, Rain has consistently reported an authorization rate of 95% to 97%, excluding expected declines. This means when a cardholder makes an intended purchase with a Rain-issued card, it goes through nearly every time. The global average authorization rate is between 85% and 95%.

Rain’s authorization rate is the result of deliberate choices about infrastructure and risk management, choices we think every cardholder and partner should understand. Let’s explore:

Rain’s design means most declines are expected

Rain is a collateral-backed credit card, meaning every transaction is backed by secured assets. If a purchase amount exceeds the available deposits, the transaction is declined. As such, the vast majority of declines on Rain-issued cards are the result of insufficient funds. These are not systemic failures, but expected, mechanical outcomes that result from how the product works.

Partners have visibility into decline reasons through Rain's reporting, so if a transaction is blocked for this reason, they can alert cardholders. Partners can also build in notification tools that flag when a cardholder’s deposits dip below a certain threshold. These include push notifications, emails, or SMS to prompt cardholders to top up their balance.

Rain’s fraud detection is effective

A high authorization rate is typically indicative of a well-designed, functional fraud detection system. Overly aggressive fraud controls are not a sign that a program is safer, but an indication that the risk models lack sophistication.

A program that blocks liberally will inevitably block some fraud, but it will also block a significant volume of legitimate transactions. The fraud reduction is a byproduct of suppression rather than detection.

At Rain, the goal is not maximum blocking, it’s precision, and getting there starts early. A significant reason why Rain’s fraud detection program is so effective is that the due diligence process is extensive. Before a program goes live, Rain completes a thorough review of the partner's business model and risk profile.

At the cardholder level, Rain employs Customer Identification Program (CIP) standards that go beyond the regulatory minimum, collecting not just identity documents but information like occupation, annual income, and IP address. This additional context helps establish a baseline for what normal activity looks like for each cardholder, so genuinely unusual behavior stands out and declines are informed by real data, not indiscriminately issued. The result is a program that doesn't treat caution and performance as competing priorities.

The bottom line

Partners don't build card programs for the infrastructure, they build them for growth. More cardholders means more spend, which means more revenue. Authorization rate is one of the most direct levers for all three.

At 95–97%, Rain's programs are performing at the top of the market. Every percentage point above average is more transactions completed, more cardholders who keep using the card, and more revenue flowing to partners.

Rain's authorization rate didn't happen by accident, and it isn’t sustained without ongoing work. If you want to learn more about how Rain approaches card issuance or explore what a partnership looks like, let’s talk.

How Rain powers Wallbit's card program for remote workers in Latin America

Remote work is reshaping economies globally, especially in Latin America (LATAM) where thousands of remote workers receive salaries in USD. Despite earning in a stable global currency, these workers often face substantial hurdles in accessing, managing, and spending their USD earnings conveniently. Traditional banking solutions often result in costly currency conversions, restrictive access, and complicated withdrawal processes, impacting financial freedom and efficiency. Wallbit, a US-based digital neobank servicing LATAM remote workers, recognized the pressing need to provide their users with a robust, frictionless, and globally accepted payment solution.

The solution

To address these challenges, Wallbit partnered with Rain to launch their Visa card program. Leveraging Rain's advanced card issuance infrastructure, Wallbit is now able to offer its users commission-free USD credit cards that simplify the process of spending and managing earnings worldwide. Key elements of Rain's solution include:

- Global spending freedom: Wallbit users receive Visa credit cards issued in the US, enabling effortless payments both locally and internationally, free from costly conversions or complicated fees.

- Simplified financial management: Remote workers can seamlessly access and utilize their USD income directly, whether paying for local expenses, traveling abroad, or subscribing to online services, all without additional taxes or charges.

- Robust security and reliability: Rain’s secure card issuance infrastructure includes advanced security measures and real-time fraud monitoring, protecting user funds and data.

- Scalable infrastructure: Rain's flexible and reliable system enables Wallbit to rapidly scale their card program, accommodating growing demand across their key markets in Argentina, Colombia, and Mexico.

The results

The collaboration between Rain and Wallbit has significantly improved financial access and usability for remote workers across LATAM:

- Empowering financial inclusion: Thousands of remote workers across Argentina, Colombia, and Mexico now enjoy unrestricted access to their USD income, eliminating previous financial barriers and creating greater financial independence.

- Reduced transaction costs: By eliminating unnecessary currency conversions and fees, users see immediate savings, improving their overall financial wellbeing.

- Enhanced user satisfaction: Wallbit has reported high customer satisfaction rates, with users valuing the ease and convenience of managing their finances through the Wallbit app and Rain-enabled Visa Platinum card.

- Increased adoption and usage: The streamlined and globally accepted credit card has driven growth in new user adoption and existing customer engagement for Wallbit, solidifying its position as a leading digital banking solution for remote workers in the region.

“Partnering with Rain has enabled Wallbit to truly unlock financial freedom for our users. Remote workers in LATAM now have seamless access to their USD earnings, without unnecessary fees or friction.” — Rodrigo Vidal, CEO of Wallbit

Conclusion

Through Rain’s innovative card issuance technology, Wallbit is successfully addressing the unique financial needs of LATAM's remote workforce. By seamlessly integrating USD-based spending and management into everyday life, Wallbit and Rain together provide remote workers freedom and flexibility, ushering in a new era where the future of work meets the future of banking.

How Rain powers Cadana’s card program for a globally distributed workforce

In emerging markets, millions of workers and businesses lack access to traditional banking infrastructure, limiting their ability to transact globally. Remote workers, freelancers, and businesses operating across borders often face challenges with payment reliability, high transaction fees, and limited access to USD-based financial tools.

Cadana, a fintech focused on financial inclusion for workers in emerging markets, sought a solution that would provide its users with secure, flexible, and globally accepted payment options. They needed a partner that could enable seamless virtual card issuance while ensuring transaction reliability and security across emerging markets.

The solution

Rain partnered with Cadana to power its virtual card program, providing users in emerging markets with a secure and efficient way to receive payments, transact online, and participate in the global economy. By leveraging Rain’s digital infrastructure, Cadana’s virtual card offering delivers:

- Seamless cross-border transactions: Rain’s technology ensures Cadana users can access globally accepted virtual USD cards, enabling payments across international platforms without friction.

- Enhanced security & fraud protection: With dynamic card details, real-time monitoring, and strict security protocols, Rain’s infrastructure minimizes fraud risks while protecting user data.

- Financial access for the underbanked: Rain’s virtual card capabilities help bridge the gap for workers and businesses without traditional bank accounts, providing them with a digital-first financial solution that works anywhere.

- Scalability & reliability: Rain’s partnership ensures Cadana can issue and manage virtual cards at scale, providing a stable and high-availability solution that meets the needs of a globally distributed workforce.

The results

With Rain’s card infrastructure, Cadana has expanded financial access for workers and businesses across emerging markets. Key outcomes include:

- Empowering financial inclusion: Thousands of users now have reliable access to virtual USD cards, eliminating barriers to global commerce and financial participation.

- Improved payment efficiency: Rain’s technology enables faster and more reliable payments for remote workers and businesses, reducing delays and transaction costs.

- Enhanced security & compliance: The partnership ensures that Cadana’s virtual card program meets the highest security standards, protecting users while maintaining compliance with financial regulations.

Conclusion

Rain’s cutting-edge card infrastructure plays a crucial role in enabling Cadana’s mission to provide financial access to workers in emerging markets. By simplifying cross-border payments and ensuring secure transactions, Rain helps drive financial inclusion and economic growth in underserved regions.