How Rain approaches wallet monitoring: Q&A with Chainalysis

At Rain, fraud prevention and detection starts long before a user attempts a transaction. One of the earliest tools we use to mitigate risk is wallet monitoring, the practice of screening where onchain value has been before arriving in a smart contract connected to a Rain-powered product. Identifying source of funds is one of the primary ways we protect the platform, our partners, and our users.

Screening at this level takes overlapping systems and specialized expertise, which is why we work with best-in-class vendors alongside our internal controls. One of these partners is blockchain analytics company Chainalysis. We sat down with Caitlin Barnett, Director of Regulation and Compliance at Chainalysis, to dig into how upstream wallets are identified and risk-scored, and why real-time monitoring is mission critical for stablecoin payment infrastructure providers like Rain.

Q: How does Chainalysis identify wallets onchain?

A: It starts with clustering, which is the process of grouping individual blockchain addresses that we can determine are controlled by the same entity. The scientific methods for grouping addresses together depend on the blockchain. On UTXO chains like Bitcoin, we use co-spend heuristics. If two addresses sign the same transaction as inputs, they share a private key and therefore belong to the same wallet. On account-based chains like Ethereum or Tron, different techniques apply, but the principle is the same and the end goal is to link addresses to their common owner. Importantly, we only leverage Machine Learning techniques for lead generation as those are probabilistic and less certain.

Once we have clusters, we layer on attribution. Our research team continuously maps clusters to real-world identities through Open-Source Intelligence (OSINT) research, law enforcement partnerships, proprietary data collection, and community submissions. That means a cluster isn't just "these 50 addresses move funds together," it's "these 50 addresses belong to VASP ABC," or "this cluster is operated by a sanctioned entity."

We also maintain address-level identifications for cases where a single address within a larger cluster has a distinct designation. For example, for a specific deposit address at a major exchange that's been listed on an OFAC sanctions designation, the parent cluster might be a legitimate exchange, but that particular address carries its own risk signal.

The result is a layered identification system: clustering tells you who controls what, attribution tells you who they are, and address-level identifications distinguish operators from users.

Q: How does Chainalysis identify risky actors?

A: We assess risk through two complementary lenses: direct identification and exposure analysis.

Direct identification is the most straightforward. If we've attributed a cluster to a known ransomware group, a sanctioned entity, a darknet marketplace, or a scam operation, that identification carries an inherent risk category. Our research team tracks these entities continuously and maintains the most comprehensive high quality database of illicit actor attributions in the industry.

Exposure analysis is where things get more nuanced. Even if a wallet doesn't belong to a known bad actor, it may have significant transactional ties to one. We analyze both direct exposure (the wallet transacted directly with a risky counterparty) and indirect exposure (funds passed through intermediaries before reaching the wallet). We break this down by risk category (sanctioned entities, stolen funds, ransomware, darknet markets, fraud shops, child exploitation material, terrorist financing, and others) and quantify it in both percentage and dollar-value terms.

On top of that, our software lets clients set custom alert rules with configurable thresholds so that a transfer triggering, say, 5% indirect exposure to a sanctioned entity fires a high-severity alert, while 1% exposure to a mixing service might be a medium. Risk isn't binary, it's a spectrum, and we give our clients the tools to define where their lines are.

Q: Why is wallet monitoring especially critical for a stablecoin payments provider like Rain?

A: Stablecoins have moved well past crypto-native use. They're now processing real payment volume: cross-border settlement, card transactions, treasury flows. That shift is exactly why regulators hold infrastructure providers to the same standard as any payments processor or money transmitter.

These regulators expect real-time monitoring, not after-the-fact reviews. A payments infrastructure provider sees the transaction as it happens, not weeks later in a batch report. If a sanctioned wallet moves funds through your platform in real time and you don't catch it, that's not a reporting gap you can close later. It's a live compliance failure, and potentially an enforcement action.

Reputation follows directly from that. A payments platform's value depends on partners, banks, and regulators trusting that every transaction moving through it has been screened, not sampled after the fact. Wallet monitoring is how stablecoin platforms demonstrate that trust is earned in real time, transaction by transaction, rather than assumed.

Q: How does wallet monitoring evolve as new chains, wallets, or laundering techniques emerge?

A: This is one of the hardest problems in the space, and honestly, it's a never-ending arms race. A few things are critical to staying ahead.

As the blockchain ecosystem grows and activity expands across an increasing number of networks, Chainalysis coverage must continuously evolve to meet customers wherever onchain activity takes place. Today, Chainalysis supports more than 30 blockchains with deep attribution and clustering coverage, supporting 3-5 new chains each quarter. Supporting a new network goes beyond technical integration and tracking value transfers. We apply existing intelligence, develop new clustering heuristics, and discover new attributions to identify the entities and types of activity occurring onchain. This gives customers the context they need to understand not just how value moves, but who is involved and what that activity represents. This is to say we're constantly onboarding new networks and deepening our analytics on existing ones.

Laundering techniques evolve constantly. Cross-chain bridges, privacy protocols, chain-hopping through DEXs, nested services with the playbook changing every few months. Our response is multi-layered: we invest in cross-chain tracing capabilities so that moving funds from Ethereum to Tron to Solana doesn't break the trail; we deploy threat detection that can flag exploit patterns and anomalous behavior even before a cluster is formally attributed; and we maintain real-time monitoring infrastructure that watches for onchain events such as fund movements, approval changes, and contract interactions at the block level.

Every new attribution, every new cluster identification, and many law enforcement cases we support feed back into the system. The compounding effect of this intelligence network is what makes monitoring more effective over time even as adversaries adapt.

Q: From your vantage point across many clients, what separates a company with a strong wallet monitoring program from one with a weak one?

A: Three things stand out consistently.

First, strong programs are proactive, not reactive. Weak programs screen a wallet when a compliance officer gets a tip or when a regulator asks a question. Strong programs screen in real time every counterparty at the point of transaction whether that's deposits or withdrawals. They also have automated alert pipelines that surface risk without waiting for a human to go looking. The difference between catching a sanctioned entity's funds before they clear versus three days later is the difference between a compliance success and an incident report.

Second, strong programs invest in tuning. Out-of-the-box alert thresholds are a starting point, not a destination. The best teams iterate on their rules by adjusting exposure thresholds by category and building tiered escalation workflows. They understand that 2% indirect exposure to a mixing service means something very different from 2% direct exposure to a sanctioned entity, and their rules reflect that nuance. Weak programs leave default settings in place and drown in noise, which leads to alert fatigue and, eventually, missed real risk.

Third, strong programs treat monitoring as cross-functional, not siloed. The best clients connect their wallet monitoring data to their broader risk and investigation workflows, which allows them to tie blockchain analytics to KYC data, case management, and regulatory reporting. They use exposure data not just to block or allow a transaction, but to understand the full risk profile of a customer relationship over time. A single suspicious transfer is data; the pattern across six months of transfers is intelligence. The companies that build that connective tissue between monitoring and decision-making are the ones that consistently stay ahead of both illicit actors and regulators.

Wallet monitoring is one piece of a larger system

Real-time screening catches what a transaction looks like the moment it happens. But a strong risk program has to hold that same standard at every other point in a payment program's lifecycle: who signs up, where they're signing up from, what changes as a relationship evolves. That's why Rain treats risk mitigation as a continuous discipline rather than a checkpoint, with clear ownership over transaction-level controls, AML and fraud risk assessment, and geographic and sanctions screening from onboarding through ongoing use.

Read more about how we structure that program in How Rain Reduces Risk: A Guide.

How Rain approaches transaction monitoring

At Rain, we monitor every single transaction that runs on our infrastructure. We screen in real-time at the authorization level, and continue reviewing payment activity as it accumulates. That coverage is the foundation of our broader fraud prevention and detection program built to protect the people and businesses who rely on our products.

Transaction monitoring systems are both the least visible and most important parts of a payments company. In the sections that follow we share information about the shape of our transaction monitoring program and the thinking behind it. We do this because openness and transparency are core to our overall approach to compliance, though of course we can’t share all the details because doing so might provide too clear a roadmap to those who might try to circumvent them.

Layered by design

Our approach to fraud prevention and detection is layered by design, because no single control catches everything. Consider how office buildings are protected. The badge reader at the entrance turns away anyone without credentials. The security officer that knows the staff catches the person who has a badge but does not belong. One is a fixed rule and the other is an awareness of what normal looks like, and removing either weakens the whole. Payments security is no different.

Transaction monitoring really starts before a Rain-powered program is even up and running. Our extensive Know Your Business (KYB) screening process helps us establish a baseline for normal program activity, including where transactions will be taking place and what payment volume will look like. Through Know Your Customer (KYC) screening, we collect cardholder details like occupation and address, information that enables us to paint an even more detailed picture of what we should expect from individuals in a program.

Activity that is normal for one program could be suspicious for another, so a single rulebook is ineffective. Picture a corporate travel program next to a payroll card program. In the first, purchases across three countries in a single week look routine. In the second, that same pattern raises red flags. Understanding each program is what allows us to spot genuinely unusual activity without turning away legitimate spending.

The next layer is at the authorization level, in the seconds between a card being presented and a purchase being approved. We monitor card activity in real-time, often catching suspicious activity as soon as a bad actor initiates it. This allows us to reject a fraudulent purchase before it even clears.

When it comes to authorization level declines, some rules are constant and apply to every program that runs on Rain. Transactions tied to sanctioned or restricted jurisdictions will always be declined, as will purchase attempts from blocked merchant categories. When spending breaks the velocity limits for a given card, merchant, or merchant category, we decline transactions. This is one of the most effective defenses against card testing and rapid-fire attacks where a bad actor will run many small charges in quick succession to find out which stolen numbers still work. Catching that burst early makes a real difference. Enhanced, custom controls can be added on top of the ones Rain requires to fit an individual program’s specific risk profile.

The next layer looks beyond any single payment. Once a transaction clears, we keep analyzing activity across the program to catch systemic risks. A group of transactions that each seemed ordinary at authorization can reveal a coordinated scheme when viewed together, and we cannot see that pattern unless we continue to monitor after settlement. Post-transaction monitoring also includes tracking disputes, refunds, and chargebacks to identify fraudulent activity. This layer is important when it comes to tracking fraud rates and the effectiveness of the entire transaction monitoring system.

These layers each work alongside network-level controls and transaction monitoring. The card networks decline transactions their models flag as unauthorized, and they intervene against patterns like BIN attacks, where fraudsters generate and test card numbers at scale.

The controls described in this section are only part of a broader program. We layer in additional rules and dynamic risk signals that adjust as behavior and threats change, and we work to anticipate new attacks rather than react to them.

Where people come in

Not everything resolves in an automated rule, and it shouldn't. When activity trips our monitoring, it goes to human review. Analysts investigate the context around it, and cases that warrant it are escalated to our Compliance team, where we make the final decisions and fulfill our reporting obligations. Automation gives the program its reach, but our skilled people give it judgment.

The honest reality of this work is that it’s never finished. Threats constantly evolve, and a program that is effective today will be tested by something new tomorrow. Our rules and risk signals adjust as behavior changes, and we devote time to studying attack patterns that have not reached us yet. Some of the controls I am proudest of were built for attacks we anticipated before they were attempted.

Transaction monitoring is just one part of a larger system. The KYB and KYC programs I mentioned above and our intensive wallet screening program are described in more detail in our guide on how Rain reduces risk. Together, each part of our risk mitigation program reflects a belief we hold across Rain. In payments, trust is the product and it has to be engineered and defended every day.

A closer look at scoped cards

Payment relationships are built on trust. Whenever you delegate spending, whether it be to an employee, contractor, vendor, or AI agent, you have to decide how much power to hand over. That choice has usually been all or nothing. You share full payment credentials and hope they're used the way you intended, or you hold them back and slow the work down.

That's why Rain developed scoped cards, making it possible to define exactly what a card can do before it's issued. Limits on spend, where the card works, and how long it’s valid are programmed into the card, creating real buying power within set boundaries.

How it works

Partners can design customized payment experiences with Rain's scoped cards offering. Scoped cards work for any situation where a person needs to delegate spending power. An expense platform can give distributed teams cards limited to travel or software. A bill-pay platform can generate a card that only works to pay specific invoices. An automated shopping platform can enable agents to initiate and execute transactions on behalf of humans.

Whatever the use case, scoped cards are the building blocks. The demo below shows just one way a partner could use scoped cards to power purchases. Click through to see the full flow in action.

The rules are set before each card is issued, and parameters can be mixed and matched across cards. A card can carry a maximum transaction amount, work only within approved merchant categories or at specific merchants, and expire after a set date. Cards could be designed to retire after a single purchase, stay active until a one-time budget is met, or refresh on a recurring budget. Each parameter is a capability, allowing cardholders to tailor the payment method to exactly what they need.

Partners can customize controls like the number of active cards a cardholder can have and daily spend limits to fit their program needs. Before a scoped card is issued, each cardholder completes KYC, the same identity verification that sits behind all of Rain’s card programs.

If you're ready to build scoped cards into your product and put precise spending controls in your users' hands, let's talk.

.webp)

Behind the buy: securing Rain’s onchain stack with Guardrail

At Rain, we’ve long held the view that security has to scale ahead of the business, not chase it.

That conviction has shaped where Rain has invested our engineering efforts, both internally and through our partnerships. A security layer has to detect threats as they happen and intervene before damage is done, and it has to do so consistently across every chain Rain operates on. The teams capable of designing and running a system like that are rare, and Guardrail is one of them.

Guardrail is the proactive, programmable security engine monitoring transactions across 30+ chains and protecting over $30 billion in assets for customers to-date. One of these customers has been Rain. Now, Rain is bringing Guardrail’s technology and team in-house to further extend real-time protection into Rain's products.

“The product is exceptional, but the team is the real reason this matters,” Rain Co-founder Charles Yoo-Naut said. “You can't put together this kind of expertise through individual hires. Samridh has assembled one of the very few groups in the world operating at that depth, and we're fortunate to have them at Rain."

Why runtime security matters

Guardrail is unique in that it defends protocols after deployment, not just before. Most security work in the blockchain industry has focused on pre-deployment audits, which are necessary but unable to catch what happens once contracts are live, where exploits move fast and often use techniques no static review can anticipate. Guardrail closes that gap with continuous runtime monitoring and automated response.

The platform works as a security engine at the base layer of every transaction. Guardrail’s AI model scores each sender, recipient, and smart contract in real time to evaluate signals like transaction value, volume patterns, approval anomalies, and oracle deviations, and then responds in under 100 milliseconds. When something looks wrong, configurable circuit breakers can halt activity before funds move. Attackers typically count on going undetected for hours, but Guardrail closes that window to near zero.

Why this matters now

This work has never been more critical. AI has changed what attackers are capable of, letting them surface exploits faster and adapt their attacks in ways defenders working with manual processes cannot match. Defending a platform like Rain against that requires the kind of continuous, automated security Guardrail has spent the past few years honing.

“We built Guardrail because the biggest unprotected surface in onchain finance isn't the code itself, it's everything that happens after it ships. More than 90% of last year's $3.4B in onchain theft hit code that had already been audited,” Guardrail Founder Samridh Saluja said. “Joining Rain takes that runtime defense to a global stablecoin payments platform where it can have outsized impact.”

What changes for Rain and its partners

By transitioning Guardrail from a vendor to an owned infrastructure layer, the enterprises who depend on Rain get a more resilient and deeply integrated service. That means runtime security scanning every transaction across all the chains Rain operates on, normalizing detection and response regardless of whether a given chain settles in milliseconds or minutes.

Ownership also compresses the time between detection and fix. When security is a vendor relationship, every iteration cycle — identifying a new attack pattern, developing a response, testing and deploying it — has to cross organizational boundaries. With Guardrail embedded inside Rain, those loops run faster and are tuned specifically for the demands of stablecoin payment flows, where the threat surface looks different than in general DeFi.

The data advantage matters too. Running Guardrail on Rain's full transaction volume gives it cross-chain context no outside vendor can accumulate. The per-contract and per-counterparty baselines sharpen with every transaction Rain processes, and that means the protection compounds as Rain scales, rather than staying static.

Rain has operated at the frontier of stablecoin payments since day one, and as that frontier expands, so does the responsibility to protect it. Bringing Guardrail in-house is the natural next step of the conviction Rain has held from the start — security has to be built into the foundation, not bolted on after the fact.

For the enterprises, neobanks, and platforms that depend on Rain, that means every transaction across every chain and every market is protected by a security layer that gets sharper over time. As Rain grows, so does Guardrail's ability to defend it.

Looking ahead

Stablecoins are already moving billions, and the bar for production-grade security is moving up with them. The enterprises building on this rail will only commit if the infrastructure underneath can defend itself in real time.

Bringing Guardrail in-house lets Rain extend that protection as the platform grows, across new chains, new partners, and new categories of stablecoin commerce. We're excited to welcome the Guardrail team and to keep building toward a payments platform where security is part of the foundation, not bolted on top.

If you're building on stablecoins and want security designed right from the start, we'd love to work with you. Please get in touch here.

Introducing Rewards

A card on its own doesn't earn loyalty; people need a reason to keep reaching for it, and the programs that grow are those that give them one. That part isn't new, but what's been missing is a way to build rewards into a card program without the usual mess of vendors and reconciliation.

So we built it ourselves. Today Rain is rolling out Rewards, allowing partners to add a fully-branded, integrated loyalty platform to their card program. This means no separate vendors to piece together or infrastructure to build out, while still being customizable.

In the US, 90% of credit card spend happens on rewards cards, but for many programs, running a rewards layer is out of reach. Loyalty usually meant bringing on a separate vendor, with its own ledger and portal, then wiring it into the card and reconciling the two against each other on a delay. It's expensive, and stitching it together often takes months. Programs that would have benefited from a rewards layer just went without.

With Rain, the rewards live in the same place as everything else. Points, earn rules, and redemption all run on the infrastructure that already handles spend and settlement, so there's no second ledger to keep in sync and no extra vendor in the middle. The points themselves are minted onchain after a transaction has settled. This means every point has a clean record, sitting in the same system that already holds the cardholder's other assets.

Everything else is the partner’s to shape. They set their own earn rules, whether that's a flat rate across the board or extra points in the categories their cardholders care about most, with room to layer in merchant-specific campaigns whenever it makes sense. Cardholders see the partner's brand, not ours, the whole way through. And when they're ready to redeem, they do it right inside the same app, either as credit against their statement or toward hotels and flights in a white-labeled travel portal. Click through the demo below to see how the integrated rewards platform could look.

We’re opening up Rewards to all partners because we know it works. Rewards are already live on Avalanche Card, and the results speak for themselves. Over 30 days, cardholders with Rewards spent about 25% more per day than those not enrolled, compared with their previous spending history.

Capturing a lift like that used to mean the expensive, slow setup most programs couldn't justify. Now it's something a partner on Rain can add on top of what they already run. And for those still picking where to build their program, it's the difference between launching a card and launching one people keep coming back to. If you’re ready to explore what your business can unlock with Rain, let’s talk.

State of stablecoins in Latin America

Last updated: June 2026

Executive summary

Latin America has emerged as one of the most dynamic stablecoin markets in the world. Between 2022 and 2025, the region recorded roughly $1.5 trillion in cryptocurrency transactions, with US dollar-backed stablecoins making up the majority of these flows, according to data from Chainalysis. By early 2025, an estimated 57.7 million people in Latin America held digital currencies, representing about 12% of the region’s total population, according to Coinchange.

Stablecoin adoption across Latin America is structural, not speculative. Stablecoins are solving concrete problems, including preserving purchasing power in high-inflation economies, reducing the cost and latency of cross-border payments, and giving individuals and businesses practical access to US dollars. Regulatory developments across much of Latin America and greater access to stablecoin-powered infrastructure platforms have also contributed to increased usage in the region.

This report examines how stablecoins are being used in practice across Latin America. It covers the structural drivers behind adoption, how use cases and adoption levels differ by country, who the key infrastructure players are, and where the regulatory landscape is heading.

Why stablecoins? The structural drivers of adoption

Stablecoin adoption in Latin America is not a product of crypto enthusiasm. It's a response to persistent gaps that traditional financial infrastructure hasn't addressed. Three forces drive the majority of usage across the region.

Force #1: Currency instability and dollar access

Several major Latin American economies have experienced periods of double- or triple-digit inflation, capital controls, or acute foreign exchange shortages. Argentina's peso has lost more than 99% of its value against the US dollar over the past decade. Bolivia's official foreign exchange reserves collapsed from a peak of $15.1 billion in 2014 to roughly $1.7 billion by 2023. The shortage led banks to sharply restrict dollar card spending and charge steep commissions on international transactions, pushing individuals and businesses toward informal markets and parallel exchange rates. In this environment, dollar-denominated stablecoins like USDC and USDT function as a practical savings instrument and a way to access US dollars.

The same logic applies at the business level. International commerce requires a shared unit of account, and USD remains that unit across the region. For companies that import goods, pay overseas contractors, or invoice international clients, holding working capital in USD-backed stablecoins eliminates timing risk on FX conversion and simplifies cross-border reconciliation.

Force #2: High fees and friction in cross-border payments

Cross-border flows between the US and Latin America are among the most economically significant — and historically expensive — payment corridors in the world. In 2024, nearly $170 billion in remittances flowed to Latin America and the Caribbean, roughly 80% of it sent from the US.

The World Bank estimates that the average cost of sending remittances to Latin America remains between 5% and 7%, depending on corridor and transfer size, with the global average sitting at 6.5% in 2025. In addition to explicit fees, senders and recipients absorb costs through foreign exchange spreads, settlement delays (typically one to three business days), and intermediary bank charges. Stablecoin-based transfers can reduce these costs substantially.

With stablecoins, remittance fees can be reduced by as much as 92%. The exact reduction amount depends on the provider; some exchanges offer 0% for stablecoin on and offramping, while others charge as much as 4.5%. A 2026 survey of 4,600 users across 15 countries found stablecoin transfers cost an average of 40% less than traditional remittance channels.

Stablecoins are also lowering costs for business-to-business cross-border payments, like contractor payroll and corporate treasury transfers. B2B stablecoin payment volume grew more than 730% year-over-year in 2025, with total stablecoin payments reaching an estimated $390 billion, more than double 2024 levels. B2B transactions now account for roughly 60% of that volume. Bitso Business reports that 45% of its total institutional stablecoin volume is for B2B and corporate treasury transactions.

Force #3: Limited banking access

Traditional banking infrastructure is fragmented across Latin America. The World Bank estimates that in 2021, 122 million adults across the region did not have access to a bank account.

Banking access has improved across many countries in the region with the rise of fintechs and digital banking services, but the range between countries remains vast:

- Mexico: According to the World Bank's Global Findex 2025, 53% of adults in Mexico had a financial account at a bank, mobile-money service, or other institution, meaning roughly 47% had no formal financial account.

- Colombia: Banking access in Colombia has expanded rapidly over the past decade. Adult account ownership rose from 30% in 2011 to 46% in 2017 and 57% by 2024, per the World Bank. Even so, roughly 43% of adults still had no formal financial account in 2024, leaving a large share of the population reliant on cash and outside the formal banking system.

- Brazil: Brazil is among the region's most banked markets, and access has risen sharply over the past decade. The share of Brazilian adults with a financial account climbed from 70% in 2017 to 84% by 2021 and 86% by 2024, according to data from the World Bank. Pix, the central bank's instant payment system launched in November 2020, has been a major driver of that shift; by late 2025, roughly 93% of the adult population used it.

A country’s specific banking infrastructure landscape shapes how stablecoins enter the market. In economies with higher unbanked populations, stablecoins can act as a parallel market alternative. In more banked markets like Brazil, where Pix has reached near-universal adult adoption, fintech platforms are increasingly connecting stablecoins to existing payment rails – letting users hold dollar-denominated balances and cash out to reais via Pix – rather than relying on stablecoins as a parallel financial system.

The cost structure: traditional vs. stablecoin rails

Beyond explicit fees, the largest hidden cost in traditional cross-border payments is prefunding. Remittance and B2B payment companies have to maintain prefunded nostro accounts — cash reserves held at foreign banks — in every country they service. With two to five days of settlement lag, a company processing $1 million a day needs roughly $2 million to $5 million sitting idle in correspondent accounts at all times, and that multiplies across every corridor. Stablecoin rails offer just-in-time funding instead: settlement takes minutes rather than days, so prefunding requirements drop significantly. In 2025, Visa announced a stablecoin prefunding pilot through Visa Direct, its global payouts platform, saying stablecoin prefunding frees businesses from parking large fiat balances in advance and lets institutions move money in minutes instead of days.

Stablecoin adoption by country

Stablecoin adoption across Latin America is not monolithic. While usage is widespread, the underlying drivers differ meaningfully by country. The following profiles highlight where adoption is concentrated and what is fueling it.

Brazil

Brazil has the largest and most structurally advanced stablecoin market in the region. Stablecoins account for approximately 90% of total crypto transaction volume in the country. Unlike markets primarily driven to stablecoins by high inflation, Brazil’s adoption is the result of a more established structural change to its economy.

A significant share of stablecoin volume in Brazil comes from commercial activity. Brazil has a sophisticated cross-border trade economy with substantial import-export activity and a large remote contractor base. Traditional wire transfers carry FX spreads and settlement delays that stablecoins meaningfully lower, making them an appealing option for businesses and payroll providers.

When payments are received, businesses often prefer to hold balances in USD-backed stablecoins rather than converting immediately to reais. This reduces exposure to currency volatility. The availability of Pix, which saw a 53% increase in payment volume year-over-year in 2024, has also created a foundation for stablecoin integration that other markets lack.

On the regulatory front, Brazil has implemented one of the most comprehensive virtual asset service provider (VASP) frameworks in the region. VASPs are required to follow the same regulatory and compliance standards as other financial institutions in the country.

VASPs are also subject to cross-border transaction limits and detailed reporting obligations on foreign exchange transactions. The central bank reclassified stablecoin cross-border transfers as foreign-exchange operations in November 2025, bringing stablecoin providers under the same reporting and transaction monitoring obligations as traditional FX operators.

Brazilian officials have floated extending the IOF (Imposto sobre Operações Financeiras) tax to stablecoin flows, which would close the regulatory gap that currently makes stablecoin rails cheaper than traditional FX channels. Industry groups representing more than 850 companies have objected, arguing it would be unlawful and would harm innovation, and in March 2026 the finance minister delayed the tax consultation amid election-year tensions with Congress. The question remains unresolved and is one of the most consequential regulatory issues in the region for 2026.

In April 2026, the central bank went further with Resolution BCB No. 561, which bars regulated electronic-FX providers – payment institutions, e-money issuers, and acquirers – from using stablecoins or other crypto to settle the offshore leg of cross-border payments. Effective October 2026, settlement with overseas counterparties must run through traditional FX operations or non-resident real accounts. Individual crypto activity is unaffected, and licensed virtual asset service providers can still use stablecoins for cross-border payments under the separate Resolution 521 framework. Analysts expect the rule to raise the cost of cross-border payments and remittances by reintroducing bank spreads, correspondent fees, and multi-day settlement where stablecoin rails had offered near-instant, lower-cost transfers.

Bolivia

Bolivia's stablecoin adoption is shaped by an acute foreign exchange crisis. Bolivia's official foreign exchange reserves collapsed from a peak of $15.1 billion in 2014 to $1.7 billion by 2023, and the country's liquid dollar reserves fell to as little as $73 million in late 2025. The limited access to dollars, plus dollar card spending caps, have forced individuals into informal markets with parallel exchange rates. In this environment, stablecoins have become a functional substitute for access to dollars.

At the business level, companies that rely on imported goods are increasingly paying foreign suppliers in USDT or USDC, acquired via peer-to-peer or over-the-counter platforms. At the consumer level, startups like Meru – a local crypto wallet built on Stellar – enable everyday stablecoin payments, allowing users to purchase at local merchants via QR codes and at global merchants via Rain-issued cards, enabling consumers to make more global purchases than they would otherwise be able to. Another major player is Takenos, a consumer financial platform that enables freelancers and contractors to receive cross-border payments, hold balances in stablecoins and other currencies, and spend or transfer funds across 20 countries.

Bolivia is one of Rain's fastest-growing Latin American markets, with card spend growing more than 6x in 2025. Nearly all of that activity is cross-border. Both businesses and consumers are using stablecoin-funded cards to buy international goods and services they can't easily pay for in local currency.

Argentina

Stablecoin adoption in Argentina is primarily inflation-driven. Years of severe inflation – which year-over-year peaked near 300% in 2024 before easing to roughly 30% in 2025 – combined with capital controls and foreign-exchange restrictions, have made dollar-backed stablecoins a default savings instrument for many households and small businesses.

The scale of that demand is broad. Argentina was the second-largest crypto market in Latin America between July 2022 and June 2025 by transaction volume, at $93.9 billion, behind only Brazil, and stablecoins make up more than half of all crypto exchange purchases in the country. Inflation, currency volatility, and capital controls push households and businesses toward dollar-linked stability for savings, remittances, and commerce.

On the regulatory front, Argentina has moved from a largely informal market toward a more defined framework. Under President Milei, attitudes toward crypto became markedly more permissive, and in 2025 the securities regulator (CNV) introduced a mandatory registration regime for virtual asset service providers. The central bank has also moved toward letting banks offer crypto services, signaling a gradual shift from peer-to-peer and exchange channels toward greater institutional participation.

Colombia

In Colombia, stablecoin usage is primarily concentrated in cross-border money movement and remittance payments. Colombia's remittance market totals roughly $10 billion annually and reaches 40% of the population, bolstered in recent years by a weak local currency, and stablecoins provide an alternative to traditional remittance providers by offering faster settlement and often lower costs.

MoneyGram debuted its stablecoin-powered app first in Colombia, citing the country's status as a major inbound remittance corridor and strong demand for dollar-linked assets amid a depreciating peso.

Beyond consumer remittances, stablecoin usage in Colombia has grown among businesses and contractors, particularly for cross-border invoicing, supplier payments, and treasury management. Colombian law requires that payments between domestic residents be settled in pesos, which limits stablecoin use in purely domestic transactions, but cross-border payments are unaffected.

Notably, 99% of purchases made with Colombian pesos on centralized cryptocurrency exchanges flow directly into stablecoins, suggesting that for most users, dollar-denominated assets are the primary reason to enter the digital asset market in the first place. Colombia ranks fifth in Latin America by total crypto transaction volume at $44.2 billion, behind Brazil, Argentina, Mexico, and Venezuela. The number of Rain-issued cardholders in Colombia has grown by 64 times since the start of 2025.

Mexico

Mexico received a record $64.7 billion in remittances in 2024, the vast majority sent from the US. It’s the single largest remittance corridor in the world, exceeding $55 billion in 2022. What makes stablecoin adoption here particularly notable is that this corridor is already one of the most competitive and liquid in global payments. Major providers like Western Union, MoneyGram, and Wise have all invested heavily in US to Mexico payments, and Mexico's SPEI instant payment infrastructure enables same-day peso settlement.

Despite this access, stablecoins are gaining meaningful market share. Stablecoins are increasingly being used for remittance payments, with Bitso Business alone processing about 10% of total US to Mexico payouts.

Stablecoins accounted for 36% of crypto purchases in Mexico in the first half of 2025, led by USDC, which is still below the Latin American average of 46%.

Uruguay

With relatively stable macroeconomic conditions and a highly banked population – about 74% of adults hold a financial account – Uruguay's stablecoin adoption is less crisis-driven and more infrastructure-led.

The country enacted legislation in 2024 (Law No. 20,345) formally recognizing virtual assets and assigning oversight to the Central Bank of Uruguay, creating one of the region's cleaner compliance pathways for exchanges and payment platforms. The regulatory clarity helped drive fintech innovation in Uruguay.

Across the region, regulatory clarity correlates strongly with institutional participation. Markets with defined supervisory frameworks, like Brazil and Uruguay, see greater integration by banks, remittance providers, and payment processors.

Key players in the region

Exchanges and institutional platforms

Bitso

Bitso is one of the largest crypto platforms in Latin America, supporting more than 10 million retail users and more than 2,000 institutional clients. Bitso processed roughly 10% of the total US to Mexico remittance market.

Bitso's institutional arm, Bitso Business, crossed $80 billion in annualized total payment volume in 2025, making it the largest stablecoin payments platform in the region. Beyond remittances, Bitso Business offers a suite of enterprise services spanning multi-currency accounts, payments, FX and FX-as-a-Service, trading, stablecoin orchestration, and treasury management across Mexico, Argentina, Brazil, Colombia, Chile, Peru, the US, and Europe. 45% of its institutional volume is for B2B and corporate treasury transactions, and stablecoin adoption among its institutional clients doubled between H2 2024 and H1 2025. Local payment flows in Mexico alone exceeded $15 billion in 2025, cementing Bitso Business as a key infrastructure provider for global companies operating in the country.

Bitso has also expanded into stablecoin issuance. It launched MXNB, a Mexican peso–backed stablecoin issued through its subsidiary Juno, and co-launched BRL1, a Brazilian real–pegged stablecoin, alongside Mercado Bitcoin, Foxbit, and Cainvest.

Ripio

Ripio is one of Latin America's largest crypto exchanges, operating across Argentina, Brazil, Mexico, and beyond. In addition to exchange services, Ripio has built out a suite of local currency stablecoins, including wARS (Argentine peso), wBRL (Brazilian real), and wMXN (Mexican peso), designed to facilitate domestic-denominated payments and cross-border settlement without requiring conversion to USD. The local stablecoin suite positions Ripio as both an exchange and an infrastructure layer for regional commerce.

Neobanks

Mercado Pago

Mercado Pago is the payments arm of Mercado Libre, Latin America's largest e-commerce platform. Mercado Pago launched MeliDolar (MUSD), a USD-backed stablecoin developed in partnership with Ripio, now available in Brazil, Mexico, and Chile. As of September 2025, over $65 million was in circulation. Mercado Libre recently discontinued its original crypto token, Mercado Coin, which was used for rewards balances on the platform. Going forward, the platform will offer rewards through MUSD.

Nubank

Nubank is the largest neobank in Latin America, with over 130 million customers across Brazil, Mexico, and Colombia. Product offerings include digital accounts, cards, lending, and investment services. Nubank added stablecoin support in December 2023 and began offering yield on USDC in January 2025, becoming one of the first financial institutions to do so in the region. USDC is the second most popular asset among customers making their first crypto purchase.

Consumer wallets and payments platforms

Belo

Belo is a major consumer fintech app operating primarily in Argentina, with expansion across Latin America. It enables users to hold stablecoins that earn yield via Aave's DeFi protocol, and to spend, transfer, or receive payment in both local currency and stablecoins. Its user base accounts for more than 8% of the region's active crypto users. Belo is notable for bridging the gap between savings, yield, and everyday spending within a single interface—a model that other platforms are beginning to replicate. Belo users access global merchants via Rain-issued cards.

Meru

Built on Stellar, Meru is one of the leading examples of real-world stablecoin adoption in Latin America. The platform enables individuals and businesses in Bolivia to access digital dollars, make local payments via QR codes, and transact globally through Rain-issued cards.

By providing access to market-based exchange rates and seamless USDC payments, Meru helps users preserve value, reduce transaction costs, and participate more effectively in both local and international commerce. The platform demonstrates how stablecoins can solve tangible economic challenges and drive financial inclusion in markets with limited access to dollars.

Takenos

Takenos is a consumer financial platform focused on cross-border money movement and global payments across Latin America. It enables freelancers and contractors to receive cross-border payments, hold balances in stablecoins and other currencies, and spend or transfer funds across 20 countries. Built on Solana, Takenos has processed over $560 million in volume and reported roughly 20% month-over-month growth throughout 2025, with a $10 million seed round co-led by Variant and Lattice. Takenos enables cross-border spending via Rain-issued cards.

Félix Pago

Félix is a WhatsApp-native remittance and financial services company built for Latino immigrants in the U.S. The company allows users to send money to Latin America as easily as sending a message, while using stablecoins such as USDC as part of its behind-the-scenes settlement infrastructure. Rather than exposing users directly to crypto, Félix leverages stablecoin rails to reduce FX and operational inefficiencies, improve settlement speed, and connect U.S. dollar flows to local payout networks across Latin America. Félix has processed more than US$6 billion in remittances and currently serves key U.S.–Latin America corridors including Mexico, Guatemala, Honduras, El Salvador, Nicaragua, Colombia, the Dominican Republic, Ecuador, and Peru.

USD vs. local currency stablecoins

Because accessing US dollars remains one of the primary reasons businesses and individuals use stablecoins, the biggest tokens used in Latin America remain USD-backed. USDT and USDC together account for more than 90% of stablecoin transfer volume on exchanges as of mid-2025. USD stablecoins rose from around 60% in 2022 to more than 90% in 2025. For most cross-border and treasury use cases, USD tokens are the natural default, offering deep liquidity, near-universal acceptance, and a shared unit of account for international commerce.

But dollar access isn't the only draw. Local currency stablecoins like BRL1, pegged to the Brazilian real, let businesses price, invoice, and settle domestically without converting to and from USD, and give consumers a more functional version of the money they already hold. The trade-off comes down to liquidity and acceptance: USD tokens offer cross-border utility but may require conversion for domestic pricing, while local tokens reduce domestic FX friction but depend on regulatory clarity and banking integration to scale. Current volumes suggest USD stablecoins will stay dominant for cross-border and treasury functions, while local tokens grow within regulated domestic ecosystems.

Conclusion

In the past few years, stablecoin adoption in Latin America has shifted from a handful of isolated use cases to one of the most diverse and active ecosystems in the world.

The adoption drivers across the region vary by country. Currency instability, expensive cross-border rails, and uneven banking access are structural features of the region's economy. As long as those conditions persist, demand for stablecoin-denominated savings, payments, and treasury management is likely to continue growing alongside the infrastructure being built to support it.

Looking ahead, regulatory changes across the region will influence how both consumers and businesses engage with stablecoins. The use cases that have taken hold across Latin America, and the infrastructure being built to support them, represent some of the clearest real-world examples of stablecoins meaningfully impacting how consumers and businesses operate financially.

Introducing the Agent Control Layer

Rain's Agent Control Layer gives businesses and developers precise, programmatic control over how AI agents spend using cards and move money on behalf of users. Partners define the conditions under which an agent can transact, and Rain enforces them before any money moves.

Agents have been transacting on Rain's infrastructure in production for months. They book travel, subscribe to software, run procurement workflows, and move money globally. To scale that activity, businesses need to bound what an agent can do, keep its activity auditable, and adjust the limits as workflows grow. The Agent Control Layer provides that framework.

The controls are enforced at card issuance and transfer initiation rather than applied after the fact. By the time an agent attempts to transact, the governing rules are already in place, and a transaction that falls outside them does not proceed.

Card controls

Rain's scoped virtual card infrastructure already supports agent purchases. The Agent Control Layer adds two levels of control on top of it.

At the agent level, users define what their agent can do before it acts: transaction amounts, merchant and category allowlists, spend intervals, and card expiry. An agent issued a card for a single booking can be limited to approved airlines or hotels, capped at a set amount, and restricted to a defined window. Outside those parameters, the card does not transact.

At the program level, partners manage risk across their entire user base, with caps on the number of active cards, aggregate spend limits, and the visibility to identify unusual activity early.

Sponge, a Y Combinator-backed company building for autonomous agents, is one of the partners issuing agent-usable cards on Rain today. Its cards are funded by a user's stablecoin balance and let agents transact anywhere Visa is accepted online, across more than 175 million merchant locations.

Money movement controls

The same controls extend across Rain's money movement suite: virtual accounts, onramps, offramps, and fiat and stablecoin payments to individuals and businesses. Partners define approved counterparties, amounts, frequency, and timing before an agent is permitted to act.

A business that enables agents to manage vendor payments can restrict those agents to approved vendors, on a defined schedule, for a defined amount. Changes to those terms require explicit action by a human administrator.

Available in beta

The Agent Control Layer is available in beta. Businesses tracking the autonomous payments category now have production-ready infrastructure and a governance framework built for machine actors, and can begin running real workflows rather than waiting for the category to mature.

It is the latest piece of Rain's ongoing work in agentic payments, which spans compliance frameworks built for autonomous actors, programmable settlement across cards, bank rails, and blockchains, and interoperability with emerging agentic commerce protocols, including early work on the open standards we believe the industry will need to build together.

Reach out to the team to book a demo.

Machine-initiated payments will unlock new opportunities for payment credentials

It’s rare for a change in consumer payments to justify rebuilding the foundation, but few innovations have been quite as disruptive as agentic commerce.

For nearly sixty years, the card payment credential, personal account number (PAN), has been a static, reusable identifier riding on rails designed for human-initiated transactions. The 16-digit account number was introduced in the 1960s as a way to extend a line of credit to a specific person at a specific bank. In the world Visa designed this in, with paper slips, carbon copies, in-person purchases at the point of sale, the design made sense. More than 60 years later, though, nearly every payment protocol still assumes the same factors in each transaction: a credential tying an account to a cardholder, a merchant, and a moment of human consent at the point of sale.

Commerce itself has changed dramatically since the 1960s. The rise of e-commerce stripped away the physical signals — a card in hand, a signature, a clerk — that the original model relied on, and the industry had to invent new ones to keep the system running. CVV2 and address verification were grafted on to stand in for physical presence. PCI-DSS set rules for how merchants could store the PAN.

EMV 3-D Secure, introduced in 2001 and refreshed as 3DS 2 in 2016, layered cryptographic authentication on top of that flow. Network tokenization, which Visa launched in 2014 and was standardized across the industry in the following years, replaced the PAN at point of use so the real account number never traveled with the transaction. Each of these was a real upgrade, and together they made online commerce workable at scale. But each was a layer wrapped around the same credential. A human still types or pastes the same 16-digit number into a checkout field, and the system still treats that act as proof of intent. E-commerce demanded changes around the credential, not to it. That work is still ahead.

When agents are the buyer, the credential has to carry more than account identity. At Rain today, this happens at issuance. Agents transact using scoped virtual cards that are customized to work at approved merchants under specific conditions. Consumers and businesses directing agents to buy on their behalf go through the same KYC and KYB procedures their cards have always required. This model operates within the rails merchants already accept, which matters because agent purchases need to land in the same checkout flows human purchases do, certainly in the near term, and likely in the future, too.

Cards, however, were not designed for what comes after this. The next wave of agentic commerce is not agents using cards to check out at the same merchants as humans, but machine-to-machine payments, where the buyer is software, the seller is software, and consent must travel inside the credential itself rather than sit at the moment of issuance. A credential whose only job is to identify an account cannot express what an agent is allowed to do; only that an account exists.

The design space for what comes next is wide open, but we see a few things as non-negotiable. An agentic payment credential needs to clearly identify the funding source behind the transaction, so issuers, merchants, and networks know who is ultimately on the hook. It needs to carry the human-approved constraints under which the agent is authorized to spend. This means which merchant, what amount, for how long, on whose behalf, under what conditions, and by what means it can be revoked. And it needs to be auditable, both for the human who delegated spend authority and for the broader set of parties — issuers, networks, regulators — responsible for consumer protection. These properties are what turns an account identifier into a record of consent.

The implications of this extend beyond the technical layer. Moving consent into the credential changes what an authorization request actually verifies, what a merchant can directly confirm about who authorized the transaction, and how disputes are resolved when the buyer is not human. This model will support microtransactions and programmatic commerce between services that current rails cannot economically serve, and allow for consumer protections that operate through constraint rather than detection. The scope of what an agent can do will be defined in advance, not inferred from behavior after the fact.

Most of the changes to consumer payments over the past two decades have been refinements within the same model. The shift that agentic commerce requires is structural; the credential has to account for who, or what, is actually transacting.

Rain integrates Monad, bringing card programs to the financial layer of the internet

Rain now supports Monad, the high-performance Layer 1 bringing parallel execution to the EVM.

A crucial component of the internet financial layer is efficient and scalable payments capabilities. This integration gives fintechs and crypto-native builders a new option for issuing cards and running high-volume payment programs.

For Rain partners looking to launch a stablecoin card, payroll product, or cross-border remittance flow, the underlying chain infrastructure needs to handle real transaction volume without fees spiking during busy periods. Monad processes transactions in parallel rather than one-by-one, which keeps costs flat and confirmations fast even when usage climbs. Monad’s architecture is designed for full functionality and money movement as volume scales.

Stablecoin-backed cards put real demands on blockchain infrastructure. Card networks operate on tight timing windows, and the onchain leg of a transaction needs to keep pace. Monad's sub-second deterministic finality is well-matched to those requirements, opening up card-native products that can compose onchain operations at the speed of a card tap.

For Rain partners building on Monad, that means a few key things:

- Predictable fees at scale, which matters when you're modeling unit economics on millions of small-ticket transactions.

- Full EVM compatibility, so any team already building on Ethereum can turn on Monad support without rewriting their stack.

- As card functionality continues to integrate blockchain technology, card authorizations will settle in well under a second, so the onchain leg never holds up the swipe.

For Rain, adding Monad is part of a broader effort to extend card-issuing infrastructure to the chains where partners are building. Each new chain integration is custom work. Our protocol engineers design and implement tailored smart contracts and outside auditors review everything before it goes live. Ongoing audits after a protocol goes live on Rain help keep the system secure as programs grow.

"Adding Monad gives builders a high-performance option without asking them to compromise on what they can launch.” Charles Yoo-Naut, Rain Co-founder and CTO, said. “Monad's architecture lines up with what consumer payments require at scale and allows us to explore new experiences only possible on the most performance chains.

Companies already building with Rain and Monad

For Monad, Rain bolsters an expanding payments ecosystem. A growing set of fintechs and payment platforms are looking to leverage Rain and Monad to bring stablecoin-powered card programs to market. These include:

- Rhythmic – building consumer payment products with embedded stablecoin rails

- Avici – developing programmable money experiences and stablecoin-native financial tools

These teams are actively building with Monad’s high-throughput, low-latency infrastructure, combined with Rain’s card issuing stack, to unlock new categories of real-world payment applications.

Adding Monad to the Rain platform reflects continued demand from partners looking to build on infrastructure that can support the workloads consumer payments produce.

“The Rain integration opens up more optionality for businesses and retail users alike to use Visa cards on Monad,” Raj Parekh, Head of Stablecoins and Payments at Monad Foundation, said. “Sub-second onchain transaction finality is critical in order for card issuers and neobanks to scale stablecoin card activity and this is something Monad uniquely unlocks.”

Know Your Agent: the next layer of compliance

If you ask most compliance teams who their customer is, they should be able to tell you instantly. Ask them who the agent transacting on behalf of their customer is — what model powers it, how it fails, what it’s authorized to do — and you will likely be met with silence.

Whether or not compliance teams are aware or prepared, autonomous actors are participating in the global economy today. Agents are buying concert tickets, executing stock trades, booking flights, and moving money on behalf of a human that may be thousands of miles away from the IP address placing the order.

The compliance frameworks built on top of today’s payment rails were written for a world where a human authorized every transaction, but the world is changing.

How will LLMs behave under pressure? What failures will surface as agentic commerce scales? Where does liability sit when the entity transacting isn't human? The honest answer is we don’t know, at least not fully. What we do have is a framework that’s worked for decades, and a starting point for how to extend it.

At Rain, our founding principle for scaling agentic commerce is simple: Know Your Agent is an extension of Know Your Customer. This isn’t theoretical; Rain is powering agentic commerce partners and use cases today, and our due diligence process is now based on this standard when onboarding partners that support agentic purchases for users.

What does the Know Your Agent process look like? Before we onboard an agentic program, we evaluate the LLM that’s powering it. We look at how that model tends to behave and where it fails. An Anthropic-powered agent does not act identically to an OpenAI-powered one, and the differences matter.

We also require the partner to explain the agentic use case and walk us through how the agents will actually operate — the number of cards needed, the typical spending pattern of the agent, and where we should expect activity to occur are all essential details. From there, we build an agent profile. This is a behavioral baseline of what we expect to see, so that when an agent deviates from it, unusual activity and fraud stand out.

Of course, the agent profile only matters if it stays anchored to a human. Agents are not onboarded as new, independent entities; they are extensions of the customer. Just like human actors, though, agents are not perfect. They have vulnerabilities, and they do act in ways that are somewhat independent.

Compliance and risk teams across the industry are going to have to reconcile with this, and it’s top of mind for us at Rain. "The agent did it" can't become a catch-all loophole for cardholders, and at the same time, the framework has to leave room for legitimate errors that aren't fraud.

One of the most challenging realities is that agentic commerce is, in many ways, fundamentally at odds with long-standing fraud controls. Rapid transaction patterns and purchases from many different IP addresses simultaneously are classic indicators of illicit activity. Both are also inherent to how agents operate.

We are adapting our transaction monitoring to be able to distinguish between sanctioned agent behavior and genuine fraud, and we layer in program-level controls to keep that distinction enforceable. This includes things like caps on active agent cards, on cards created per day, and on total agent spend per user. When something does slip though — and it will — the potential for loss is much higher, so our detection and reaction time needs to be immediate.

AI is changing how money moves, and compliance teams have to be willing to sit with the hard questions this reality presents. At Rain, we’re compelled by the technical innovation, and we’re leaning in to build the compliance infrastructure that has to come with it. We believe in our foundation, and we’re putting it to work.

Rain is now a Mastercard Principal Member

Stablecoins are no longer on the fringe of global payments. The next wave is consumer spending and everyday business payments, and the infrastructure supporting that wave needs to be trusted, scalable, and global.

Today, Rain is announcing our Mastercard Principal Membership. This means that Rain can now offer credit and prepaid cards on the Mastercard network, giving our partners greater flexibility, control, and choice as they scale their stablecoin-powered payment programs.

What this means for our partners

Partners building global card programs need infrastructure that can meet them where their users are, and where their business is going.

Rain's infrastructure stack was purpose-built for stablecoin card programs, not retrofitted from a fiat model, and allows programs to expand across geographies through a single integration rather than rebuilding market by market. Partners get to market faster, and scaling after launch is simpler.

Mastercard is accepted by hundreds of millions of merchants across more than 210 countries and territories. That reach will now be available to Rain partners.

Settlement modernized behind the scenes

Beyond card issuance, Rain and Mastercard will explore settling select program flows onchain using regulated stablecoins. This matters because settlement can be capital-intensive and create operational constraints.

Traditional fiat models rely on fixed banking cut-off times and require partners to pre-fund several days of spending volume in reserve at all times, tying up liquidity and reducing flexibility. Rain’s infrastructure already supports daily settlement with card networks including weekends and holidays, cutting that collateral requirement significantly. Onchain settlement, once implemented, would take that further, supporting more frequent, always-on settlement while improving capital flow and keeping the cardholder experience exactly as it should be.

From the cardholder’s perspective, nothing changes. Cards continue to deliver the familiar, secure, and globally accepted experience they’re expected to. Stablecoins do the work in the background – strengthening settlement and liquidity flows rather than altering the moment of payment itself.

Part of something bigger

This announcement builds on Rain's recent selection as a launch partner in the Mastercard Crypto Partner Program, which brings together innovators across the digital assets ecosystem to advance onchain payments. Through the program, and now as a Principal Member, Rain and Mastercard will collaborate to explore new integrations, co-develop payment capabilities, and expand real-world stablecoin use cases.

It also follows Rain's $250M Series C, which we raised to accelerate exactly this kind of work: network integrations, international expansion, and new products that make stablecoin payments work everywhere.

The bigger picture

Tokenized money is the next era of money. Stablecoins are moving from niche instrument to core infrastructure, and the world's largest payment networks are moving with them.

From day one, Rain has believed that tokenized money must be usable in everyday life. Becoming a Mastercard Principal Member is another step toward making that real.

If you're building a card program and want to explore what Rain’s dual-network membership means for your business, let's talk.

Putting digital assets to work: Lydian launches a Rain-powered card program

Historically, digital assets rarely move outside of crypto wallets. Lydian is changing that.

Backed by Tether and Cantor Fitzgerald, they've built infrastructure for merchants across nine countries to offer a "Pay with Crypto" checkout option, so customers can pay directly from their wallet and merchants settle instantly in local currency. Now, they're expanding that reach with a new offering.

The Lydian Card, powered by Rain, plugs stablecoins and other digital assets into Visa’s global network, making them spendable at more than 150 million merchants worldwide. For crypto holders, getting access to that network, without converting to fiat first, changes what digital assets can actually do.

Lydian cardholders fund their accounts with stablecoins or another supported asset, and can tap, swipe, and check out just like they would with any other payment card, all while using their digital asset balances.

Merchants do not have to change anything about their checkout flows; they can use the same point-of-sale systems and they receive payments in local currency. The stablecoin infrastructure works entirely behind the scenes.

Lydian users have the option to receive virtual and physical cards, and because it’s a Visa Platinum Card, it’s a premium experience. Cardholders have access to a broad suite of benefits, including built-in car rental insurance, purchase protection on eligible items, extended warranty coverage, and 24/7 Visa customer service.

"Mainstream adoption happens when the underlying technology becomes invisible. We built Lydian to make spending digital assets feel as familiar as tapping a card at your favorite local shop,” Carl Grimstad, CEO of Lydian, said. “The Lydian Card now gives anyone that owns a digital asset—and most specifically Tether holders—the ability to use their stablecoins anywhere Visa is accepted.”

“By combining Rain's world-class stablecoin infrastructure with the premium benefits of a Visa Platinum Card, our users can now put their assets to work without ever having to worry about the complexity of conversion or settlement behind the scenes," Grimstad added.

Rain handles the infrastructure that connects Lydian's users’ stablecoin-backed spending power to Visa's network, enabling frictionless transactions and daily onchain network settlement behind the scenes, including on weekends and holidays. For partners like Lydian, this means less idle capital tied up in reserve balances, and faster time to market.

“The best infrastructure disappears, and Lydian understood that from day one,” Farooq Malik, CEO & Co-founder of Rain, said. “Now their users can use digital assets exactly how they’d spend fiat currency.”

Rain is committed to building the infrastructure that makes digital assets work in the real world. The Lydian Card is what that looks like in practice.

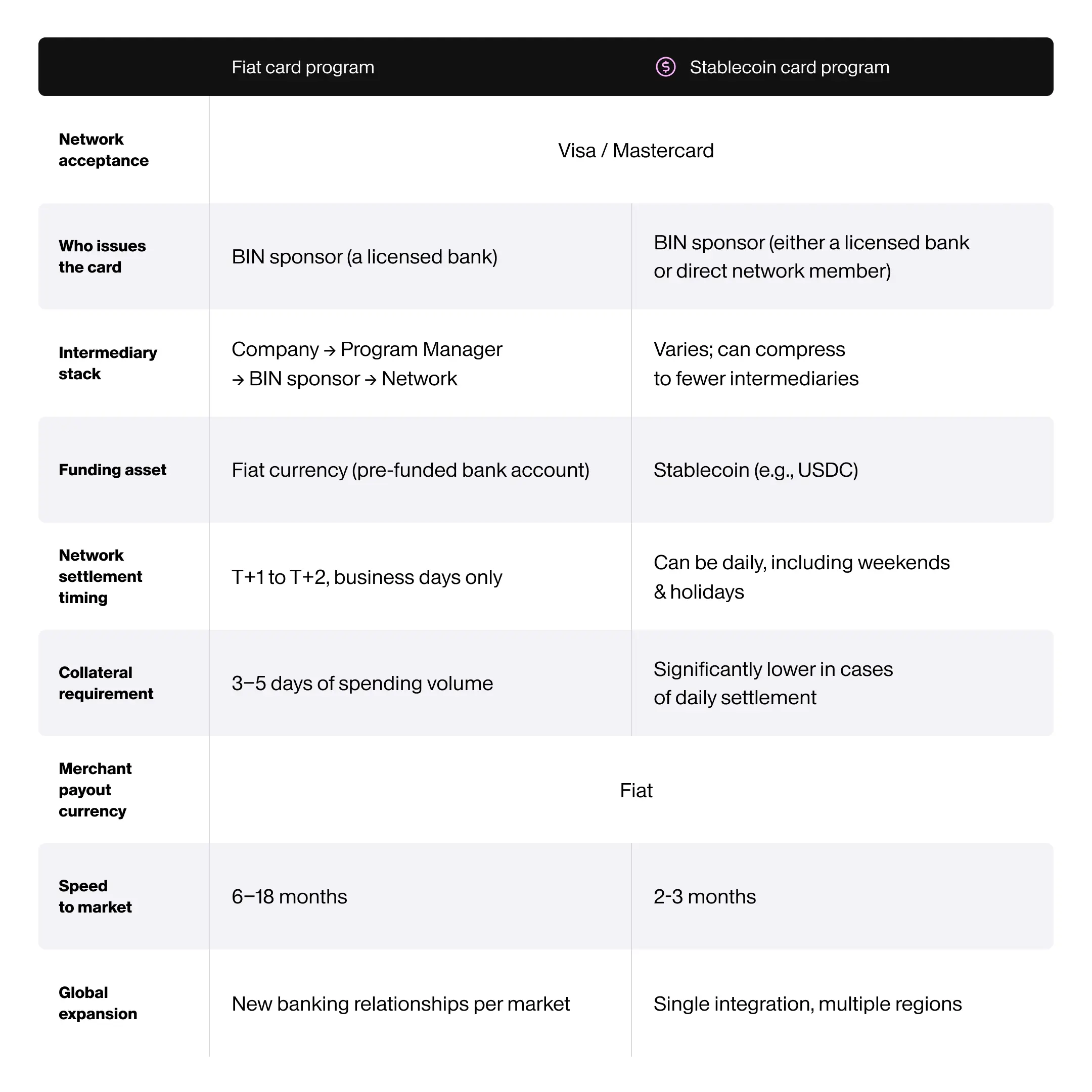

Fiat vs. stablecoin cards: what the difference means for your business

Key takeaways

- Stablecoin card programs can go live in 2-3 months vs. 6-18 months for fiat programs

- Rain’s daily onchain settlement with card networks cuts partners’ collateral requirements significantly compared to the multi-day float required for fiat programs

- Rain-issued programs scale across geographies through a single integration, so partners are not required to rebuild in each market

- The benefits apply to any business looking to launch card programs, not just crypto-native companies

The default for businesses looking to launch a card program has long been the fiat-backed model, but that’s starting to change.

Stablecoin card programs are gaining traction, and not just from crypto-native companies. Fintechs, payroll providers, and global apps that once opted for traditional fiat setups are starting to consider an alternative model, and for good reason.

For cardholders and merchants, stablecoin-backed cards and fiat-backed cards are nearly identical. Transactions are seamless, acceptance is unchanged, and nothing about the payment flow feels new or unfamiliar.

The differences are structural, and they show up in the places that matter most to a business, like how much capital a program ties up, how long it takes to launch, and what it takes to expand internationally. The decision to go with a stablecoin or fiat model shapes the entire economics and footprint of a program from day one. Here’s how:

The stack: who's behind a card program

While fiat and stablecoin programs differ at the ledger and settlement layers, both are built on top of the same card network infrastructure. Let’s get to know these key components before explaining the differences:

- The card network: Payment networks, like Visa and Mastercard, set the rules. They maintain the acceptance infrastructure, facilitate settlement between card issuers and merchants, and authorize transactions. To issue cards that work on the network, companies need to be a licensed network member, which comes with capital requirements, compliance standards, and other ongoing obligations.

- The BIN sponsor/issuing bank: Every card has a Bank Identification Number (BIN), which is the first six to eight digits on the card. BINs are assigned to licensed entities that are network members.

- The program manager: Between your company and the BIN sponsor, there is often a program manager. This is a third-party team that handles technical integration, card management, branding, and day-to-day operations.

Key differences between stablecoin & fiat programs

Difference #1: settlement and reserve requirements

It makes sense to start with the settlement layer, because this is the biggest economic burden on a business.

In a traditional fiat card program, a company must maintain a pre-funded balance, known as an FBO (“for benefit of”) account, with their issuing bank. Settlement with the card network typically takes two business days. Because of that lag, the company has to keep three to five days of projected spending volume in reserve at all times.

Rain’s card programs operate on a different timeline, from both the fiat model and other stablecoin-powered models. Rain settles with the network in stablecoins every day, including weekends and holidays. Since funds move daily, partners don’t need to pre-fund several days of spending, and capital reserve requirements drop significantly.

Rain's integrated virtual accounts and onramps allow partners to fund programs in stablecoins or fiat currency, so businesses that want to benefit from the efficiencies that stablecoins provide without holding stablecoins themselves have the option. This setup is particularly helpful for companies that want to modernize their card infrastructure without changing how they manage their existing finances.

This is one of the most significant benefits of a stablecoin-backed model. If two card programs can produce a similar end-user experience, but one requires materially less idle capital to support settlement, the difference goes beyond a technical distinction and becomes an economic advantage.

Difference #2: program expansion and USD access

Issuing cards globally is one of the most strategic ways a business can expand its financial offerings, particularly when it comes to high-demand US dollar-denominated cards. But just as settlement infrastructure can be a barrier to entry, the expensive and complicated process of expanding internationally can be prohibitive for businesses.

In markets around the world, businesses and consumers actively seek access to dollar-denominated spending, but because most fiat programs are effectively limited to a US market, there are few options.

The reason is structural. Fiat programs are often built on local banking infrastructure, and many banks in international markets cannot support USD-denominated card programs. Foreign currency exchange regulations and limited access to the US dollar clearing system make running these programs expensive and challenging.

Even when international banks can offer a USD-denominated card program, there are unique underwriting timelines, capital requirements, and approval processes in different regions. Companies with international programs also need to maintain pre-funded FBO accounts in each country.

Stablecoin infrastructure can offer a different path. Because reserves can be held in dollar-backed stablecoins rather than relying entirely on local fiat banking infrastructure, a stablecoin-backed card program can be designed to scale across markets more efficiently. That does not remove compliance obligations or local considerations, and it should not be framed as though it does. What it can do is reduce some of the fragmentation that makes conventional fiat expansion so operationally heavy.

Rain holds network membership and operates across multiple regions through a single integration, so a program that launches in one market can extend to others without rebuilding from scratch.

For companies thinking about the addressable market, global demand for dollar cards isn’t a future opportunity. It exists today, and it’s largely underserved because the fiat infrastructure required to reach it is too fragmented and slow to build. Stablecoin card programs can streamline the process, giving businesses a faster path to expansion.

Difference #3: speed to market

Speed to market is another area where the difference between fiat and stablecoin programs becomes tangible.